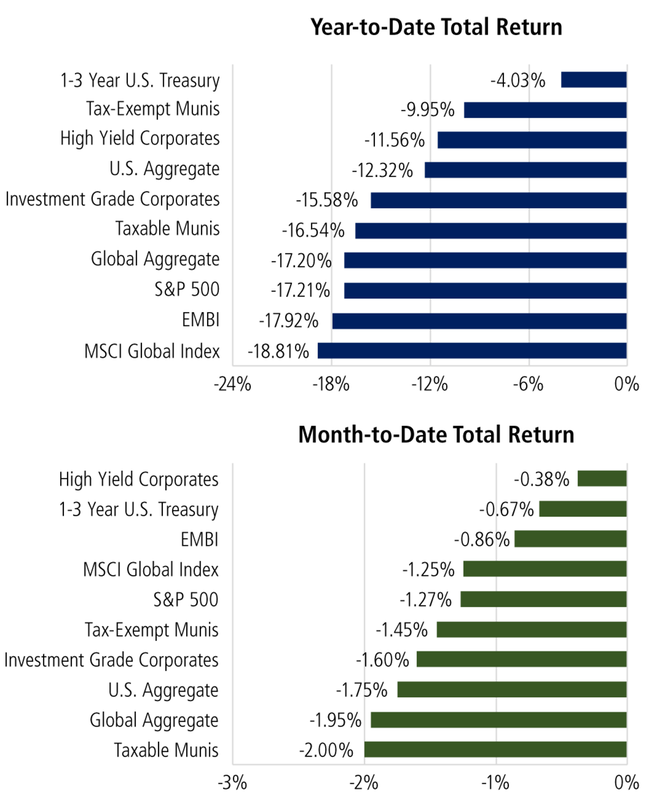

2022 brought a tumultuous year with significant losses across asset classes spurred by seven rate hikes by the Fed, 40-year high inflation, recession worries, geopolitical tensions, and supply chain disruptions. It is no surprise that stocks fell far more than the worst possible outcome forecast by Wall Street and marked the largest broad market equity decline since 2008. Market volatility was also elevated on the year with the S&P 500 dropping over -5% on four monthly occasions and jumping +5% on three monthly occasions. Given the many headwinds, it is also not surprising the S&P 500 dropped into bear market territory (> -20%) on three different periods in 2022. The biggest equity market index loser for the year was the tech-laden Nasdaq which plummeted -33%, followed by the S&P 500 which delivered a total return of -18%. Even the Aggregate US Core Bond index was clobbered with a record setting -13% loss in 2022.

Looking back to our 2022 Market Outlook, we outlined many headwinds and negative return probabilities: “we have lower expectations than past years and expect choppy U.S. equity markets... with downside risk of -9%. For perspective, the past few years we did not foresee downside volatility and therefore did not provide a range-bound forecast.” Further, we noted “risk is elevated by headwinds in the form of rising prices, higher cost of money (rates higher), slower economic growth and no more Fed or Government stimulus in play. The 2022 investment environment is further compounded with unknowable outcomes related to the potential for new lethal virus variants and escalating geopolitical risks, particularly Russia & China.”

With respect to some highlighted investment strategies in last year’s “2022 Equity Market Forecast” we noted: “Rising rates and inflation have an inverse impact (loss) on bond prices. Therefore, we will look to reduce traditional fixed-income allocations, which also have already partly been executed to some degree and look to replace with treasury inflation-protected securities (TIPs). We will also increase asset class exposure to real assets (gold, commodities, and real estate), loss buffer ETFs, absolute-return funds, along with increasing specific stock/sectors plays.”

In hindsight, a good amount of our 2022 cautionary investment thesis was on point with cutting fixed income while adding to our liquid alternative funds and real assets, including sharply overweighted positions in commodities (COMT) and energy (XLE). We also took several risk-off tactical portfolio adjustments to client portfolios in the first quarter (Q2FY22) as early inflationary signs appeared more robust and stickier than the Fed and Treasury were conveying.

Our top four equity allocations were liquid alternative funds which we coined as the “four horsemen” and which overall delivered a meaningful asset class gain that was instrumental to client portfolios: Catalyst/Millburn Hedge Strategy (+7.7%), Standpoint Multi-Asset Investor (+3.4%), Grant Park Multi Alternative Strategies (-1.9%) and Campbell Systematic Macro (+30.6%). During the year we upped our allocations to each one of these four horsemen into the 4-5% range. Assuming an overall 20% allocation to these four horsemen, then these overweight positions brought an amalgamated positive return attribute of +2% to the client portfolios on the year. Similarly, our outsized allocations to energy and commodities, up +64% and +19% respectively, brought additional resiliency during these turbulent times.

Looking back to our 2022 Market Outlook, we outlined many headwinds and negative return probabilities: “we have lower expectations than past years and expect choppy U.S. equity markets... with downside risk of -9%. For perspective, the past few years we did not foresee downside volatility and therefore did not provide a range-bound forecast.” Further, we noted “risk is elevated by headwinds in the form of rising prices, higher cost of money (rates higher), slower economic growth and no more Fed or Government stimulus in play. The 2022 investment environment is further compounded with unknowable outcomes related to the potential for new lethal virus variants and escalating geopolitical risks, particularly Russia & China.”

With respect to some highlighted investment strategies in last year’s “2022 Equity Market Forecast” we noted: “Rising rates and inflation have an inverse impact (loss) on bond prices. Therefore, we will look to reduce traditional fixed-income allocations, which also have already partly been executed to some degree and look to replace with treasury inflation-protected securities (TIPs). We will also increase asset class exposure to real assets (gold, commodities, and real estate), loss buffer ETFs, absolute-return funds, along with increasing specific stock/sectors plays.”

In hindsight, a good amount of our 2022 cautionary investment thesis was on point with cutting fixed income while adding to our liquid alternative funds and real assets, including sharply overweighted positions in commodities (COMT) and energy (XLE). We also took several risk-off tactical portfolio adjustments to client portfolios in the first quarter (Q2FY22) as early inflationary signs appeared more robust and stickier than the Fed and Treasury were conveying.

Our top four equity allocations were liquid alternative funds which we coined as the “four horsemen” and which overall delivered a meaningful asset class gain that was instrumental to client portfolios: Catalyst/Millburn Hedge Strategy (+7.7%), Standpoint Multi-Asset Investor (+3.4%), Grant Park Multi Alternative Strategies (-1.9%) and Campbell Systematic Macro (+30.6%). During the year we upped our allocations to each one of these four horsemen into the 4-5% range. Assuming an overall 20% allocation to these four horsemen, then these overweight positions brought an amalgamated positive return attribute of +2% to the client portfolios on the year. Similarly, our outsized allocations to energy and commodities, up +64% and +19% respectively, brought additional resiliency during these turbulent times.