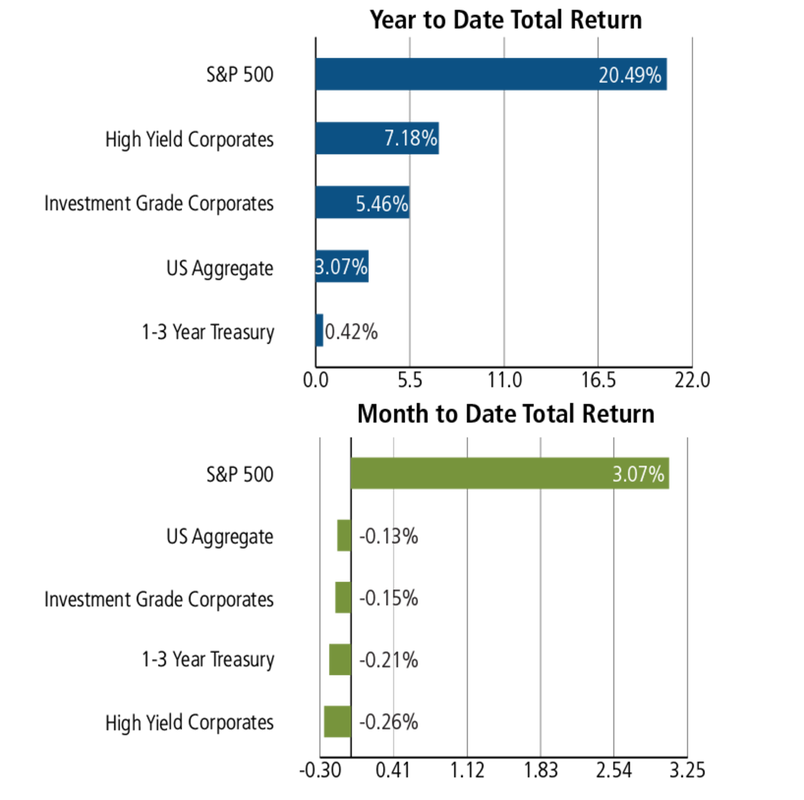

-2017 CAPITAL MARKET RETURNS: Equities, Bonds, Hard Assets, Commodities & Currency. 2017 was the second longest bull market in history and the third longest economic recovery, now into its 104th month. Clearly, we are closer to the end than the beginning, so the real question is how far we are from the end. As we enter the New Year and contemplate the opportunities the investment landscape may offer in 2018, it helps to look back at the performance trends of last year. For 2017 the broad U.S. S&P 500 gained +19.4% (w/ dividends 21.8%), the Barclay’s US Aggregate Bond Index returned +3.5%, the US Treasury 10-Yr Index returned +2.4%, gold continued its 2-year winning streak with a +11.3% gain, the Dow Jones Commodity Index returned +4.4% and US crude index was up 4.1% on the year. The stocks that have performed were in a very narrow band for 2017 — mostly social media stocks. Indeed, more than a quarter of the S&P 500’s climb is attributed to just five stocks, known as FAANG — Facebook, Amazon, Apple, Netflix and Google — have dominated the market. The so-called FAANG stocks are fetching prices that would make the Nifty Fifty blush. Their average P/E ratio is a whopping 115, compared with 22.5 for the S&P 500.

December 22, 2017 Weekly Market Roundup. Equities edged higher on the week as investor focus continued to be on the passage of the U.S. tax bill. For the S&P 500, energy shares led the gains, helped by a rise in oil prices. The prospect of an uptick in economic growth and wider deficits pushed the yield on the 10-year Treasury note to its highest level (2.50%) since March. Tax reform has largely been geared toward cutting corporate taxes, and the 2017 Tax Cut and Jobs Act will do just that – the corporate tax rate will fall from 35% to 21%.

-December 15, 2017 Weekly Market Roundup. Stocks were higher for the fourth consecutive week as investors continued to process tax reform traction and increased M&A news. Also, all major equity indices set new record highs as investors remained bullish heading into year-end. The best performing sectors were Telecom and Tech, while Utilities and Materials were the laggards. The Fed hiked rates again this week by +0.25%, from 1.25% to 1.50%. This recent rate increase marks the Fed's third interest rate hike this year and the fifth rate rise of this hiking cycle. The median policymaker “dot” for 2018 suggests three more such rate increases in the year ahead.

-December 8, 2017 Weekly Market Roundup. The S&P rose +0.35% and the Dow Jones rose +0.4% for the week, while the Nasdaq continued to lose ground, slipping -0.1% for the week. 2017's return makes it the third-best year of this bull market and the sixth-best year in the past two decades. The week’s jobs report marked the 86th consecutive month the U.S. economy has experienced positive job growth by adding 228,000 jobs in November; higher than the expected 195,000. Investors also welcomed news that both the Senate and House approved a two-week funding bill, staving off a threatened government shutdown this weekend.

-December has historically been the most bullish month for U.S. stocks since the 1950s by posting gains about 75% of the time with an average return of about +1.6% for the month. This month also has never been a fallen angle with being categorized as the worst performing month for S&P 500 returns in any one year.

-December 1, 2017 Weekly Market Roundup. The U.S. equity market rallied for the second consecutive week with all major U.S. equity indices hitting record highs. The positive market tone was largely driven by optimism surrounding tax reform, increase in oil prices after OPEC extended its curbs on oil output till 2018 and initial jobless claims hit a near 45-year low. Revised third quarter growth (GDP) came in higher at 3.3% annualized, higher than the 3.2% print expected; the highest since the third quarter of 2014. High yield markets were down -1.3% through the middle of November before recovering to return -0.3% for the month. Fed Chair resignation speech offered positive insights: “As I prepare to leave the Board, I am gratified that the financial system is much stronger than a decade ago, better able to withstand future bouts of instability and continue supporting the economic aspirations of American families and businesses.”

December 22, 2017 Weekly Market Roundup. Equities edged higher on the week as investor focus continued to be on the passage of the U.S. tax bill. For the S&P 500, energy shares led the gains, helped by a rise in oil prices. The prospect of an uptick in economic growth and wider deficits pushed the yield on the 10-year Treasury note to its highest level (2.50%) since March. Tax reform has largely been geared toward cutting corporate taxes, and the 2017 Tax Cut and Jobs Act will do just that – the corporate tax rate will fall from 35% to 21%.

-December 15, 2017 Weekly Market Roundup. Stocks were higher for the fourth consecutive week as investors continued to process tax reform traction and increased M&A news. Also, all major equity indices set new record highs as investors remained bullish heading into year-end. The best performing sectors were Telecom and Tech, while Utilities and Materials were the laggards. The Fed hiked rates again this week by +0.25%, from 1.25% to 1.50%. This recent rate increase marks the Fed's third interest rate hike this year and the fifth rate rise of this hiking cycle. The median policymaker “dot” for 2018 suggests three more such rate increases in the year ahead.

-December 8, 2017 Weekly Market Roundup. The S&P rose +0.35% and the Dow Jones rose +0.4% for the week, while the Nasdaq continued to lose ground, slipping -0.1% for the week. 2017's return makes it the third-best year of this bull market and the sixth-best year in the past two decades. The week’s jobs report marked the 86th consecutive month the U.S. economy has experienced positive job growth by adding 228,000 jobs in November; higher than the expected 195,000. Investors also welcomed news that both the Senate and House approved a two-week funding bill, staving off a threatened government shutdown this weekend.

-December has historically been the most bullish month for U.S. stocks since the 1950s by posting gains about 75% of the time with an average return of about +1.6% for the month. This month also has never been a fallen angle with being categorized as the worst performing month for S&P 500 returns in any one year.

-December 1, 2017 Weekly Market Roundup. The U.S. equity market rallied for the second consecutive week with all major U.S. equity indices hitting record highs. The positive market tone was largely driven by optimism surrounding tax reform, increase in oil prices after OPEC extended its curbs on oil output till 2018 and initial jobless claims hit a near 45-year low. Revised third quarter growth (GDP) came in higher at 3.3% annualized, higher than the 3.2% print expected; the highest since the third quarter of 2014. High yield markets were down -1.3% through the middle of November before recovering to return -0.3% for the month. Fed Chair resignation speech offered positive insights: “As I prepare to leave the Board, I am gratified that the financial system is much stronger than a decade ago, better able to withstand future bouts of instability and continue supporting the economic aspirations of American families and businesses.”