July 19, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA. Amid tech-stock rout, the S&P 500 and Nasdaq posted the sharpest weekly losses since April. The S&P 500 shed 2% for the week, while the Nasdaq dropped 3.6%. The indexes have tumbled amid a selloff in chipmakers and other large-cap technology stocks. Microsoft (MSFT) disrupted many operating systems around the world after a coding error by cybersecurity provider CrowdStrike (CRWD) crashed, thereby paralyzing airlines, trading systems, courts, and other critical services.

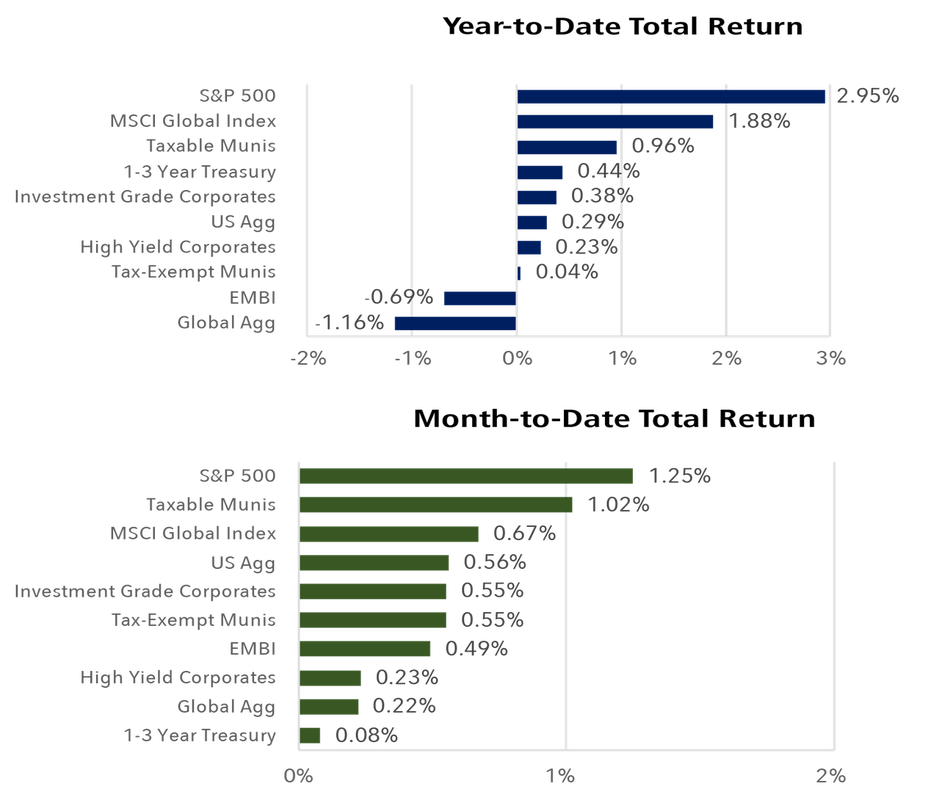

July 12, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA. All three major US equity indexes finished with gains for the week, led by Dow Jones with slightly more than 2%, followed by the S&P 500 nearly reaching a 1.5% gain, and the Nasdaq setting a new high with almost a 1% weekly gain. June also marked the second consecutive month of soft inflation readings, with the June Consumer Price Index (CPI) report showed core CPI eking up only 0.06% over the month. There are a number of positive factor inputs that are driving the positive returns for stocks in 2024:

July 12, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA. All three major US equity indexes finished with gains for the week, led by Dow Jones with slightly more than 2%, followed by the S&P 500 nearly reaching a 1.5% gain, and the Nasdaq setting a new high with almost a 1% weekly gain. June also marked the second consecutive month of soft inflation readings, with the June Consumer Price Index (CPI) report showed core CPI eking up only 0.06% over the month. There are a number of positive factor inputs that are driving the positive returns for stocks in 2024:

- The GDPNow model estimate for real GDP growth (seasonally adj annual rate) in the 2Q 24 is 2.0% on July 10, up from 1.5% on July 3

- GDP growth in the United States is projected to be 2.6% in 2024

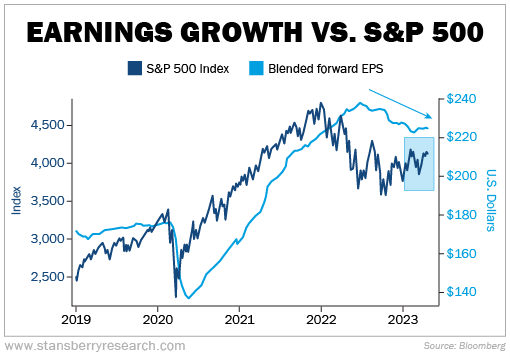

- SPX is expected to report Y/Y earnings growth of 8.8% for Q2 2024

- CY 2024, analysts are calling for (year-over-year) earnings growth of 11.0%

- Interest rate curve forward contracts show 90% chance Sept rate cut & second rate cut to November, with about even odds of a third rate cut by year's end

- S&P Dow Jones Indices expects S&P 500 companies to repurchase $885 billion in stock in 2024

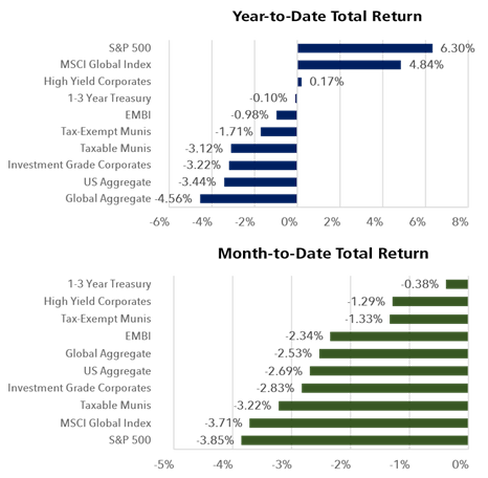

July 5, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA. Stocks rallied on the week led by tech-laden Nasdaq +3.5%, followed by the Dow Jone +0.7% and the S&P 500 +0.5%. Nevertheless, the S&P faces increased concentration risk as the broad market index nears 17% year-to-date, with just five stocks responsible for 63% of the S&P's return in the current year. The latest employment report for June revealed a surge in unemployment up to 4.1%, nearing a level not seen in three years, which has intensified the pressure for the Federal Reserve to consider implementing interest rate reductions come September. The market's confidence in the timing of a Fed cut strengthened Friday, as the futures contract-implied odds of a September cut rose to 75%, up from 64% a week ago, and the chances of two or more rate cuts by the end of 2024 climbed to 71%, up from 63% a week ago, according to CME FedWatch Tool.