-April 27, 2018 Weekly Market Update. Major U.S. market equity indexes traded largely flat to slightly down for the week while the economy notched another quarter of growth for the first quarter, growing +2.3% at a quarter-over-quarter annualized rate (beating the 2.0% estimates). The U.S. economy has grown at a healthy +2.9% clip year-over-year. Yet, the S&P 500 showed no traction for the week by ending flat, while the Dow Jones and Nasdaq lost -1.03% and -0.37%, respectively. Not even strong S&P 500 corporate earnings that have exceeded 20% has been a sufficient enough catalyst to reset the bull market trend. This level of earnings growth is a remarkable achievement during a period where many are calling for a bear market. Indeed, these factual positive fundamentals are antithetical to Bloomberg’s call of a bear market based on “People who expect the stock market to fall over the next year now outnumber people who predict the opposite.” So far for the first quarter, 79% of S&P 500 companies have beaten EPS estimates to date. If 79% is the final percentage for the quarter, it will mark the highest percentage since we began tracking this data in 2008. Technology leaders Facebook, Amazon, Alphabet and Microsoft also all reported significant revenue for the week.

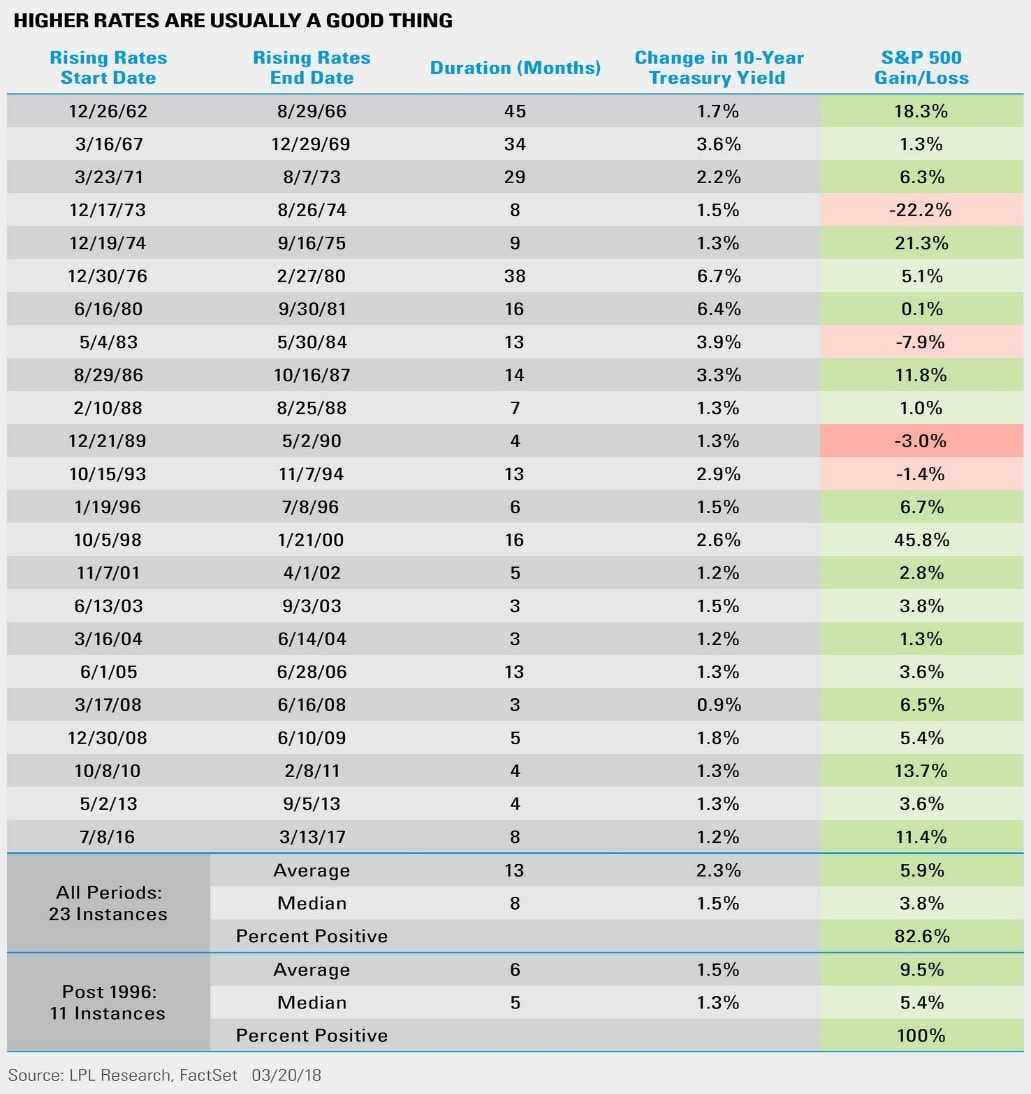

-April 25, 2018 Market Research Note. The yield on the 10-year Treasury note, which helps set rates for auto loans, mortgages and other lending, climbed to 3 percent for the first time since 2014. Some strategists have predicted the 3 percent 10-year yield represents the end of the stock market rally, with corporate borrowing costs becoming too punitive and fixed-income looking too appealing. The view is higher rates would be a drag on the economy and therefore a harbinger for both economic woes and stock market upheaval. The corollary to this theory is higher rates are bad for stocks period? To the contrary, since the early '60s we've seen periods of higher rates 23 times and the S&P 500 was higher 19 of those times (Refer chart below). It is also our view we are in a market environment of higher growth and higher interest rates - while these early stage conditions are often supportive to equity valuations - these two factors are also often associated with more market volatility. Again, investors (& their advisors) should take this opportunity to review asset allocations relative to age, goals, and tolerance for risk and volatility.

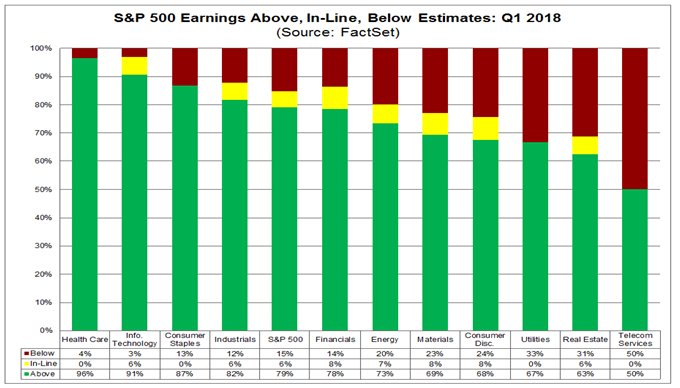

-April 20, 2018 Weekly Market Update. The U.S. equity market barely nudged through to its second consecutive weekly gain, with the S&P 500 Index ($SPX) rising +0.26% and a +0.45% year-to-date total return. Strong corporate earnings growth of 18.3% for the first quarter helped alleviate the sharp market jitters; also, so far this has been the highest earnings growth since Q1 2011 (19.5%). Further, $SPX is reporting a net profit margin of 11.1% for Q1, the highest net profit margin for the index since FactSet began tracking this data in 2008. Thus far, 85 companies in the $SPX have reported results and of these, about 70% have met or exceeded analysts’ sales estimates and 87% have met or exceeded analysts’ earnings per share (EPS) estimates. Despite slightly higher equity prices, there has been a cautious tone to the market over geopolitical headwinds and domestic political uncertainty. We are hopeful that next week's reported earnings for over 170 companies in the S&P 500 Index will finally establish some positive tailwind based on solid fundamentals. Indeed, company first quarter earnings results for next week include: Verizon, Lockheed Martin, Visa, United Parcel Services, Starbucks, ExxonMobil, Alphabet (parent company of Google), Facebook, Amazon, Microsoft, Intel, among others.

-April 13, 2018 Weekly Market Update. The U.S. equity markets recovered some ground this week with the S&P 500, Dow Jones & Nasdaq returning +2.04%, +1.80% and +2.77%, respectively, on positive trade statements by China, Facebook CEO Zuckerberg’s well-handled congressional testimony and positive corporate earnings developments. Case in point, China’s Xi Jinping showed promising strides in trade while 70% of S&P 500 ($SPX) companies have beaten EPS estimates to date for first quarter - equal to the 5-year average. Additionally, 73% of $SPX companies have beaten sales estimates to date for Q1, well above the 5-year average (57%). [Earnings source: Factset]

-April 13, 2018 Weekly Market Update. The U.S. equity markets recovered some ground this week with the S&P 500, Dow Jones & Nasdaq returning +2.04%, +1.80% and +2.77%, respectively, on positive trade statements by China, Facebook CEO Zuckerberg’s well-handled congressional testimony and positive corporate earnings developments. Case in point, China’s Xi Jinping showed promising strides in trade while 70% of S&P 500 ($SPX) companies have beaten EPS estimates to date for first quarter - equal to the 5-year average. Additionally, 73% of $SPX companies have beaten sales estimates to date for Q1, well above the 5-year average (57%). [Earnings source: Factset]

-April 7, 2018 Weekly Market Update. It was a wild ride for stock investors this week and I can say from my own experience as a professional investment advisor, the client calls and emails finally spiked during this week. However, given the broad market index (S&P 500) ups and downs – many of which moved into the black and red multiple times on certain days – investors might be surprised to learn that the CBOE Volatility Index (VIX) was not that far out of line with long-term trends. Indeed, the VIX (aka fear index) long-term average is 20, but during this week’s market swings the VIX only really traded between 19-25 - closing at 21.5 for the week. What also might be surprising to investors is that with two of the week's daily loses being greater than -2.0% for the S&P 500 (including Friday), the domestic broad market index only lost -1.3% for the week. Unfortunately, economic and corporate fundamentals were overshadowed by disruptive trade tariff policies [Refer to our March 3, 2018 Trump Tariff Viewpoint]. It is our view that Trump is likely using the new $100 billion of China Tariffs as a negotiation tool, as echoed by his chief economic advisor Kudlow. Regardless, there remains at least another month-and-half before any decision is made either way, including a period of CEO comments and consultation. Another mitigating circumstance is that the US is no longer a manufacturing country with about 80% of GDP tilted toward service industries. Yet, there is still a lot at stake politically with the mid-term House of Representative elections where the Republicans need every vote. Trump can ill-afford a brewing trade war that could cause economic headwinds and continued capital market unrest. Further, it is not lost on Trump that China happens to also hold about $1.17 trillion in American treasuries. Turning back to the equity markets, seven of the eight largest global companies by market capitalization come from the tech sector, and we continue to view their continued outperformance as unsustainable. Hence, other factors beyond trade war rattling is in play here. For example, the FAANGs and other emerging tech stock leaders have their own unique operational challenges that have surfaced and this just happens to be coinciding with macro global trade joisting. On the positive side, we are moving into first quarter earnings and this should be a bright spot for stocks in the news cycle. Another consideration is stock dividends have registered a +9% increase in the first quarter and it is estimated after we close second quarter of 2018, dividend payout would have reach $400 billion, with a large part expected to be reinvested in the market; thus, there is some degree of support mechanism in place.

-April 3, 2018 Market Update. This equity market research note is released before the market open today and futures have been up in the +0.60%-0.80% range. We reiterate that volatility typically extends for several months after the initial market correction (Feb 9th) and there is nothing unusual about this current cycle. The S&P 500 hit correction territory again yesterday when it tested the 2,556 level at 2:40pm EST; it also broke through -3% level loss. However, this consolidation phase of retesting the Feb 9th correction level demonstrated that there remains enough buyer interest at this market support range to drive a partial market recovery from the lows (S&P 500 finished the day at -2.23%). There are competing factors in play including: the market is correcting frothy valuations and is still processing a change to higher economic growth together with higher interest rates. Also, investor feverish sentiment toward stocks like the FAANGs - and other similar new tech like Tesla and Nvidia – had priced values to perfection in market segments that are not immune to challenges. Of course, Trump tariffs and trade war talk has only added more controversy and uncertainty in the equation – two ingredients abhorred by market bulls. From another perspective the market does great when information is being processed about higher company earnings, lower corporate taxes, higher economic GDP and infrastructure investment. Now that the discussion is about trade wars, regulations in social media, higher interest rates impact on the economy, flattening of the yield curve – then, that narrative has imputed caution back into play. We remind investors that timing the market in or out is not a strategy, nor is panicking. Also, while no one knows how long these markets will behave badly, we suggest investors (& their advisors) to use this volatility for buying opportunities and/or rebalancing allocations back in line with the long-term risk/return tolerance targets.

-April 2, 2018 Market Update. At least richly priced and overvalued equities are no longer the banner being waved by market bears as the elevated forward looking price-earnings ratio ("P/E") for the S&P 500 has sharply dropped from above 18x, to 16.1x today. This P/E coincidentally is the same P/E of the five-year average (also 16.1). Additionally, the estimated S&P 500 earnings growth rate for the first quarter 2018 is 17.3% and should this rate materialize, then this would mark the highest earnings growth since Q1 2011 [Source: FactSet]. What has driven the increase in the bottom-up EPS estimate for Q1 2018 and the entire year of 2018? The decrease in the corporate tax rate for 2018 due to the new tax law is clearly a significant factor in the upward revisions to EPS estimates. However, inasmuch as there has yet to be a sign that volatility has abetted history has proved that patient investors are rewarded with the best investment opportunities during bull markets that are afflicted with a market correction.

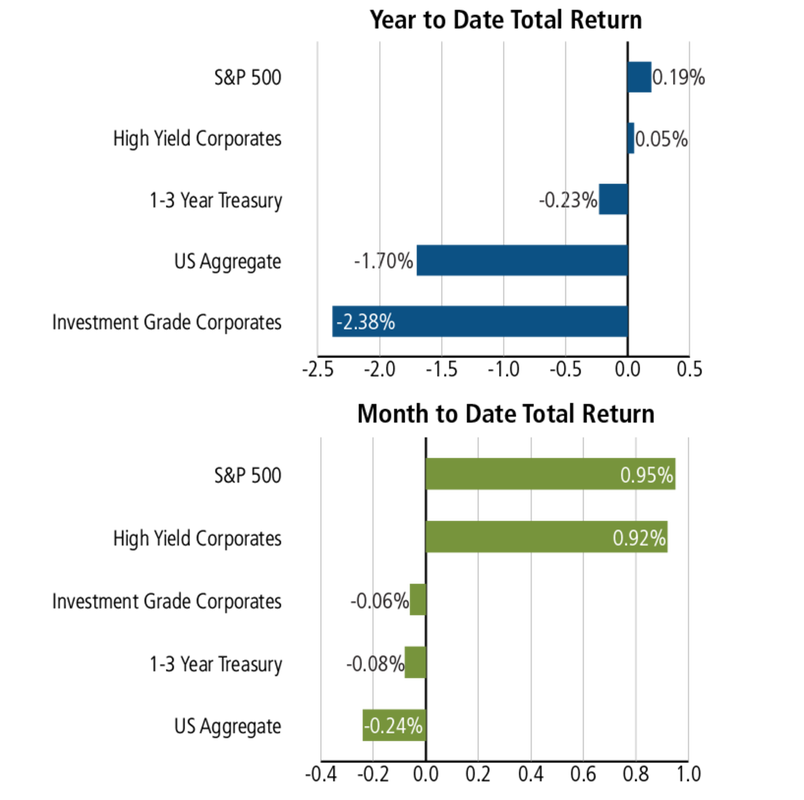

-April 1, 2018 Market Update. To the chagrin of most U.S. investors their quarterly broker statements will likely show the first loss since 2015 given both equities and bonds lost ground year-to-date. In fact, almost all investment asset classes struggled through a turbulent and volatile quarter in the capital markets. For example, the broad S&P 500 stock index fell -1.2% in the first quarter of 2018, snapping a nine-quarter stretch of gains. And, it wasn’t just domestic equities that took lumps during the quarter, as MSCI Europe also lost -2.0%, US Corporate Bond Index -2.2%, Bloomberg Aggregate Municipal Bond Index -1.1%, U.S. Intermediate Government Bond Index -1.7% and Ishares 3-7 year treasury -2.3%. Even silver and natural gas lost -4.8% and -7.4%, respectively. The most pain however was inflicted to those income-driven investors chasing high yield in master limited partnerships (MLPs) and for those investors that were naïve enough to have high weightings in MLPs probably experienced losses of around -9% for that asset class. Conversely, for those investors exposed to diverse multi asset portfolios - as employed in most of our clients' holdings - the ride should have been less wild and the losses more muted. For example, Pimco All Asset Fund eked out a gain, while certain alternative funds (like CPLSX +1.76%, JRSTX +1.57%, YCGEX +2.01%) all showed gains. Also, the preferred share holdings were largely flat and our largest bond holding of PONAX lost only -0.32%. Most of our individual client stock allocations have high exposure to defensive industries with higher yields and therefore have greater moat protection during volatile periods. For instance, industries like telecom, consumer staples and banks were also in the black so far this year. Going forward, we look for the first quarter earnings to start in this upcoming week of April and we expect positive double-digit growth; this highly visible and measurable source of positive data should help alleviate part of the market jitters associated with February and March (however, it will take a couple weeks before there are enough S&P companies reporting to have a consensus upward trend).

-April 3, 2018 Market Update. This equity market research note is released before the market open today and futures have been up in the +0.60%-0.80% range. We reiterate that volatility typically extends for several months after the initial market correction (Feb 9th) and there is nothing unusual about this current cycle. The S&P 500 hit correction territory again yesterday when it tested the 2,556 level at 2:40pm EST; it also broke through -3% level loss. However, this consolidation phase of retesting the Feb 9th correction level demonstrated that there remains enough buyer interest at this market support range to drive a partial market recovery from the lows (S&P 500 finished the day at -2.23%). There are competing factors in play including: the market is correcting frothy valuations and is still processing a change to higher economic growth together with higher interest rates. Also, investor feverish sentiment toward stocks like the FAANGs - and other similar new tech like Tesla and Nvidia – had priced values to perfection in market segments that are not immune to challenges. Of course, Trump tariffs and trade war talk has only added more controversy and uncertainty in the equation – two ingredients abhorred by market bulls. From another perspective the market does great when information is being processed about higher company earnings, lower corporate taxes, higher economic GDP and infrastructure investment. Now that the discussion is about trade wars, regulations in social media, higher interest rates impact on the economy, flattening of the yield curve – then, that narrative has imputed caution back into play. We remind investors that timing the market in or out is not a strategy, nor is panicking. Also, while no one knows how long these markets will behave badly, we suggest investors (& their advisors) to use this volatility for buying opportunities and/or rebalancing allocations back in line with the long-term risk/return tolerance targets.

-April 2, 2018 Market Update. At least richly priced and overvalued equities are no longer the banner being waved by market bears as the elevated forward looking price-earnings ratio ("P/E") for the S&P 500 has sharply dropped from above 18x, to 16.1x today. This P/E coincidentally is the same P/E of the five-year average (also 16.1). Additionally, the estimated S&P 500 earnings growth rate for the first quarter 2018 is 17.3% and should this rate materialize, then this would mark the highest earnings growth since Q1 2011 [Source: FactSet]. What has driven the increase in the bottom-up EPS estimate for Q1 2018 and the entire year of 2018? The decrease in the corporate tax rate for 2018 due to the new tax law is clearly a significant factor in the upward revisions to EPS estimates. However, inasmuch as there has yet to be a sign that volatility has abetted history has proved that patient investors are rewarded with the best investment opportunities during bull markets that are afflicted with a market correction.

-April 1, 2018 Market Update. To the chagrin of most U.S. investors their quarterly broker statements will likely show the first loss since 2015 given both equities and bonds lost ground year-to-date. In fact, almost all investment asset classes struggled through a turbulent and volatile quarter in the capital markets. For example, the broad S&P 500 stock index fell -1.2% in the first quarter of 2018, snapping a nine-quarter stretch of gains. And, it wasn’t just domestic equities that took lumps during the quarter, as MSCI Europe also lost -2.0%, US Corporate Bond Index -2.2%, Bloomberg Aggregate Municipal Bond Index -1.1%, U.S. Intermediate Government Bond Index -1.7% and Ishares 3-7 year treasury -2.3%. Even silver and natural gas lost -4.8% and -7.4%, respectively. The most pain however was inflicted to those income-driven investors chasing high yield in master limited partnerships (MLPs) and for those investors that were naïve enough to have high weightings in MLPs probably experienced losses of around -9% for that asset class. Conversely, for those investors exposed to diverse multi asset portfolios - as employed in most of our clients' holdings - the ride should have been less wild and the losses more muted. For example, Pimco All Asset Fund eked out a gain, while certain alternative funds (like CPLSX +1.76%, JRSTX +1.57%, YCGEX +2.01%) all showed gains. Also, the preferred share holdings were largely flat and our largest bond holding of PONAX lost only -0.32%. Most of our individual client stock allocations have high exposure to defensive industries with higher yields and therefore have greater moat protection during volatile periods. For instance, industries like telecom, consumer staples and banks were also in the black so far this year. Going forward, we look for the first quarter earnings to start in this upcoming week of April and we expect positive double-digit growth; this highly visible and measurable source of positive data should help alleviate part of the market jitters associated with February and March (however, it will take a couple weeks before there are enough S&P companies reporting to have a consensus upward trend).