-May 29, 2018 Weekly Capital Market Update. The CBOE Volatility Index (Ticker: VIX) or “Fear Index” spiked 29% today on geopolitical news of escalating concerns over Italy's political party coalitions which, in turn, jittered Italian bank stocks and bonds along with other EU country markets. With most overseas markets closing in the red, our U.S. markets likewise opened and subsequently closed with losses on the day. Emerging market bonds also took it on the chin for the day, while flight to quality drove the US Dollar (USD) and treasuries upward. Leaders of the far-right League and anti-establishment Five Star Movement in Italy failed to form a coalition government over the weekend and these concerns around support for populist parties gaining traction ahead of new elections has resulted in risk-off market sentiment. It is our view that while Italy's economic problems are far more severe than the political issues these are really not new developments - they have been known and priced into the markets. Indeed, Italy has been a sore spot in the EU for years and there have been a number of occasions in the past where fears of Italy splitting from the EU have surfaced – much like Greece. Yet, in the intermediate and longer-term, it has turned about to be ‘much ado about nothing.’

-May 25, 2018 Weekly Capital Market Update. While the third week of May imputed a degree of uncertainty by US policy makers, which in turn led to a mixed performance on the five trade days by US equity markets throughout the week, all major US market indexes nonetheless were able to eke out a positive return: S&P 500 +0.33%, Dow Jones +0.18% and Nasdaq +1.08%. The US stock market was exposed to counterweighing factors of influence with the positive development of Secretary Mnuchin announcing early in the week that the U.S. and China are “putting the trade war on hold,” then later in the week (Wed) where the Commerce Department put a NAFTA tariff bullseye on auto imports by stating that auto imports “threaten to impair the national security.” Then on Thursday, Trump again rattled the capital markets by calling off the peace summit with North Korea due to “tremendous anger and open hostility” on the side of Kim Jong Un. Also on the Macro-front, news surfaced on Friday of prospects for an increase in oil production by OPEC and Russia, which led the best performing S&P 500 sector (energy) to consolidate downward. In short, geopolitical headlines and Trump tweets once again overshadowed the constituent fundamentals of the 500 companies trading on the S&P index. What is becoming more and more evident is the less the President tweets and the less Trump goes off script with the media, the better the chances the underlying stocks in the S&P 500 have to meaningfully benefit from positive economic and corporate fundamental trends.

-May 19, 2018 Weekly Capital Market Update. All U.S. major equity indexes lost ground on the week with the S&P 500 -0.47%, Dow Jones -0.36% and Nasdaq -0.66%. Higher interest rates weighed on market sentiment, particularly in the rate sensitive areas of the market such as real estate, utilities, and telecom – all which lost over -2.5% for the week. Looking at future quarters, analysts currently project earnings growth to continue at double-digit levels through the end of 2018. For example, for Q2 2018, analysts are projecting earnings growth of 18.8% and revenue growth of 8.4%. Further, negative EPS guidance is 57% (51 out of 89), which is well below the 5-year average of 72% (Factset). We expect companies in the S&P 500 with higher global exposure to benefit from the tailwinds of a weaker U.S. dollar and higher global GDP growth. The forward 12-month P/E ratio is 16.4, which is only slightly above the 5-year average of 16.1. Wall Street’s consensus bottom-up target price for the S&P 500 is 3084.39, which is +14% above the closing price of 2713.

-May 25, 2018 Weekly Capital Market Update. While the third week of May imputed a degree of uncertainty by US policy makers, which in turn led to a mixed performance on the five trade days by US equity markets throughout the week, all major US market indexes nonetheless were able to eke out a positive return: S&P 500 +0.33%, Dow Jones +0.18% and Nasdaq +1.08%. The US stock market was exposed to counterweighing factors of influence with the positive development of Secretary Mnuchin announcing early in the week that the U.S. and China are “putting the trade war on hold,” then later in the week (Wed) where the Commerce Department put a NAFTA tariff bullseye on auto imports by stating that auto imports “threaten to impair the national security.” Then on Thursday, Trump again rattled the capital markets by calling off the peace summit with North Korea due to “tremendous anger and open hostility” on the side of Kim Jong Un. Also on the Macro-front, news surfaced on Friday of prospects for an increase in oil production by OPEC and Russia, which led the best performing S&P 500 sector (energy) to consolidate downward. In short, geopolitical headlines and Trump tweets once again overshadowed the constituent fundamentals of the 500 companies trading on the S&P index. What is becoming more and more evident is the less the President tweets and the less Trump goes off script with the media, the better the chances the underlying stocks in the S&P 500 have to meaningfully benefit from positive economic and corporate fundamental trends.

-May 19, 2018 Weekly Capital Market Update. All U.S. major equity indexes lost ground on the week with the S&P 500 -0.47%, Dow Jones -0.36% and Nasdaq -0.66%. Higher interest rates weighed on market sentiment, particularly in the rate sensitive areas of the market such as real estate, utilities, and telecom – all which lost over -2.5% for the week. Looking at future quarters, analysts currently project earnings growth to continue at double-digit levels through the end of 2018. For example, for Q2 2018, analysts are projecting earnings growth of 18.8% and revenue growth of 8.4%. Further, negative EPS guidance is 57% (51 out of 89), which is well below the 5-year average of 72% (Factset). We expect companies in the S&P 500 with higher global exposure to benefit from the tailwinds of a weaker U.S. dollar and higher global GDP growth. The forward 12-month P/E ratio is 16.4, which is only slightly above the 5-year average of 16.1. Wall Street’s consensus bottom-up target price for the S&P 500 is 3084.39, which is +14% above the closing price of 2713.

-May 11, 2018 Weekly Capital Market Update. All major U.S. equity market indexes rallied on the week with the S&P 500 +2.49%, Dow Jones +2.51% and Nasdaq +2.67%. The markets were uplifted with the easing of inflationary concerns after both the consumer price index (CPI) & producer price index (PPI) came in lower than expected. Markets were also supported by corporate earnings results where almost 80% of the S&P 500 $SPX companies have beaten EPS estimates to date for first quarter. If 78% is the final percentage for the quarter, it would be the highest rate since Factset began tracking this data in 2008. The energy sector has been particularly helpful to the S&P 500 with its continued recovery and this has been a standout supporting constituent of companies for the domestic broad market index. Case in point, since the end of March the S&P Energy sector has gained +14%. Finally, the dollar stabilized while the 10-year treasury was held below 3%. We view the month of May as pivotal since it can be a telling month. For example, since the 1970’s, the full year S&P 500 return has been green 35 out of 36 years that saw the S&P 500 up year-to-date in May. Hence, we are encouraged with volatility (VIX) trending below the normal range of 13-15 coupled with majority of the trade days posted gains for the week.

-May 4, 2018 Weekly Market Update. The week ended on a positive note for stocks marked by fluctuating index prices for the major U.S. equity indexes. However, even after the leading U.S. market indexes rallied strongly on Friday, stocks finished mixed for the week. The S&P 500 lost -0.21%, the Dow Jones down -0.19% and the Nasdaq recovered +1.26% on the week. The April jobs report was broadly positive while the unemployment rate fell to 3.9%, the lowest since December 2000. Further, the Fed inflation gauge for rate increases was adjusted toward greater flexibility with “symmetric 2 percent objective over the medium term.” The term “symmetry” suggests more dovish stance on Fed rate hike actions on the draconian 2% inflation target; hence, if inflation exceeds 2% the Fed may not act as aggressively.

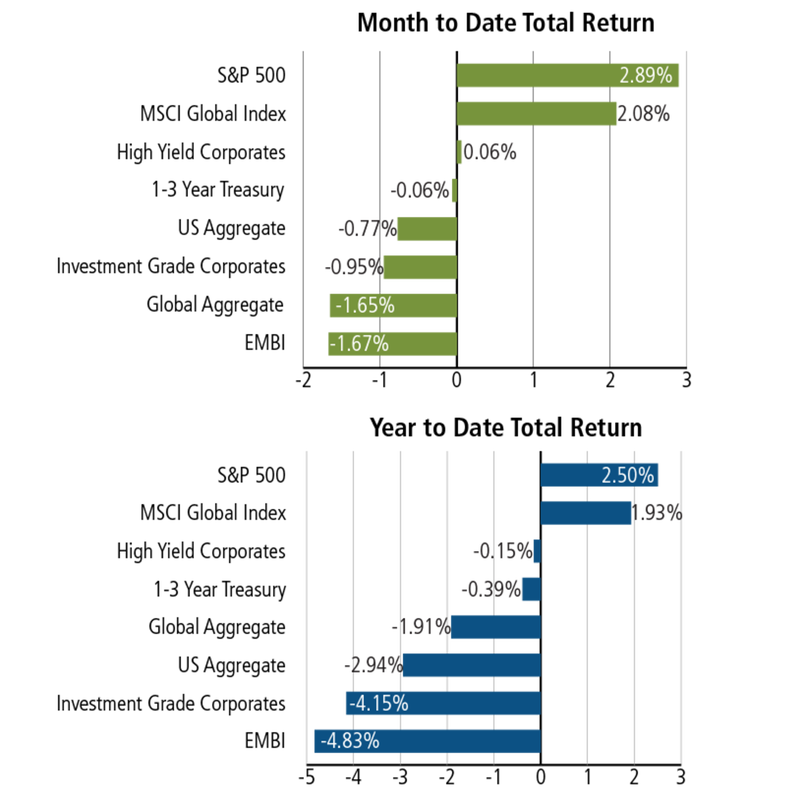

-May 2, 2018 Market Research Note: The capital markets are currently struggling to reconcile two narratives of robust economic growth and fears of increasing (downside) tail risk. There are also end-of cycle worries about growth momentum facing headwinds with higher rates and simmering trade-war undercurrents. Higher inflationary mechanisms have also resurfaced (CPI, commodities, gasoline) and there appears to be bond yield backup where yields rise, prices fall. Recall, the Fed’s March Minutes: “some further firming of the stance of monetary policy as likely to be warranted” and “that it remained appropriate to follow a gradual approach to raising the target range for the federal funds rate.” Finally, investors are also still trying to process that while equity markets are a bit off their past lofty levels, we remain in a low-return environment. Hence, as the risk-free rate moves higher, even in an orderly incremental manner, then fixed income will becomes more of a competitive asset class at some point. As for client portfolios, we will continue to implement changes to reflect all these considerations and discuss the rationale for new recommendations during our client meetings.

-Going forward, we will continue to provide capital market insights but reserve some of our more proprietary recommendations and opinions to the form of exclusive communications with our clients. More specifically, this would pertain to recommended portfolio construction changes based on new developing fundamental, economic, corporate and political considerations.

-May 4, 2018 Weekly Market Update. The week ended on a positive note for stocks marked by fluctuating index prices for the major U.S. equity indexes. However, even after the leading U.S. market indexes rallied strongly on Friday, stocks finished mixed for the week. The S&P 500 lost -0.21%, the Dow Jones down -0.19% and the Nasdaq recovered +1.26% on the week. The April jobs report was broadly positive while the unemployment rate fell to 3.9%, the lowest since December 2000. Further, the Fed inflation gauge for rate increases was adjusted toward greater flexibility with “symmetric 2 percent objective over the medium term.” The term “symmetry” suggests more dovish stance on Fed rate hike actions on the draconian 2% inflation target; hence, if inflation exceeds 2% the Fed may not act as aggressively.

-May 2, 2018 Market Research Note: The capital markets are currently struggling to reconcile two narratives of robust economic growth and fears of increasing (downside) tail risk. There are also end-of cycle worries about growth momentum facing headwinds with higher rates and simmering trade-war undercurrents. Higher inflationary mechanisms have also resurfaced (CPI, commodities, gasoline) and there appears to be bond yield backup where yields rise, prices fall. Recall, the Fed’s March Minutes: “some further firming of the stance of monetary policy as likely to be warranted” and “that it remained appropriate to follow a gradual approach to raising the target range for the federal funds rate.” Finally, investors are also still trying to process that while equity markets are a bit off their past lofty levels, we remain in a low-return environment. Hence, as the risk-free rate moves higher, even in an orderly incremental manner, then fixed income will becomes more of a competitive asset class at some point. As for client portfolios, we will continue to implement changes to reflect all these considerations and discuss the rationale for new recommendations during our client meetings.

-Going forward, we will continue to provide capital market insights but reserve some of our more proprietary recommendations and opinions to the form of exclusive communications with our clients. More specifically, this would pertain to recommended portfolio construction changes based on new developing fundamental, economic, corporate and political considerations.