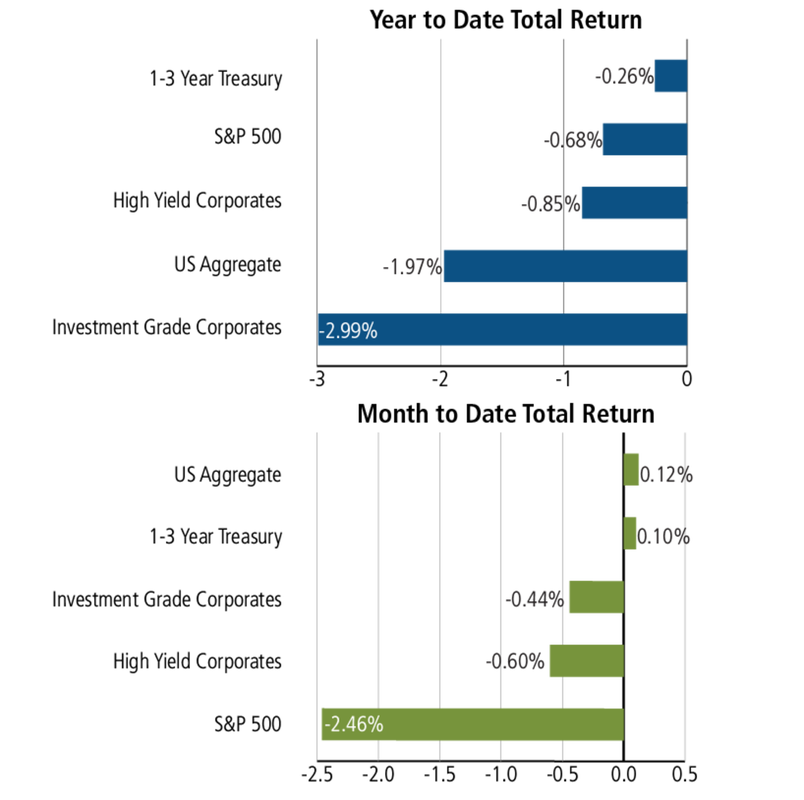

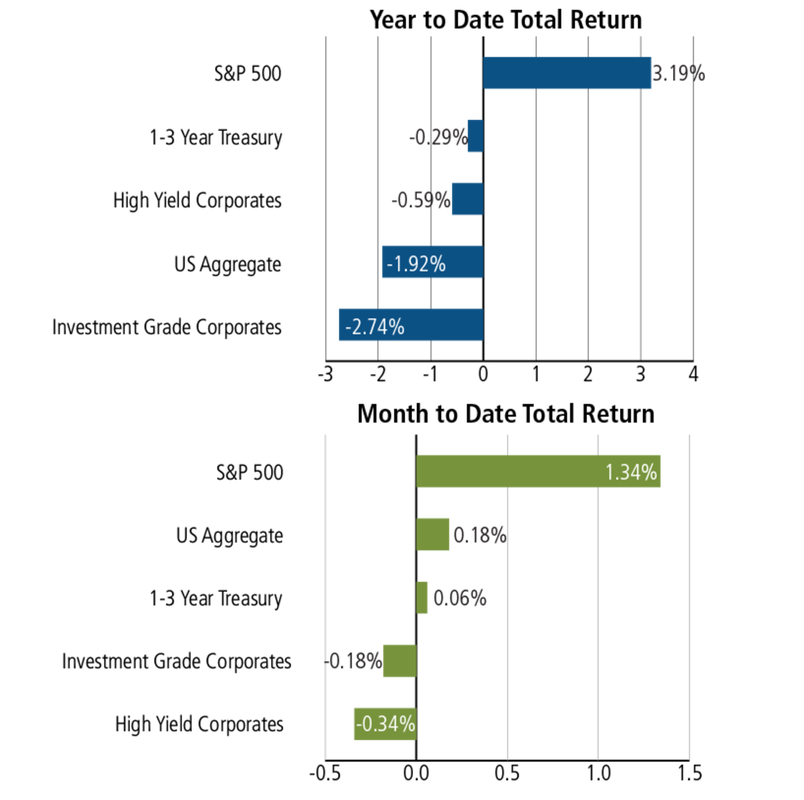

-March 30, 2018 Weekly Market Update. Markets are closed today in observance of Good Friday. It was a volatile week in the capital markets, but Thursday’s strong finish essentially was a day of recovery where all major equity indices moved back to break-even or in the black for the week. However, the S&P 500 Index still lost -2.7% for the month of March, which follows February’s -3.9% pullback; these were the first consecutive monthly declines in the broad equity Index since October 2016. As clarified in the many equity blog comments this week, the market rout originated from the sharp losses by popular (mainstream) technology names like Facebook, Twitter, Amazon, Netflix, Google, etc. However, investors can still find order in disorder by taking a broader perspective. Indeed, it should come to no surprise the hot hand in tech favorites were exposed to some degree of reversion to the mean. For example, since 2015 the Nasdaq has returned 49.1% compared to 28.3% for the S&P 500® Index. On the economic front the IMF released another silver lining by revising up its forecast for 2018 global growth by +0.2% to 3.9%.

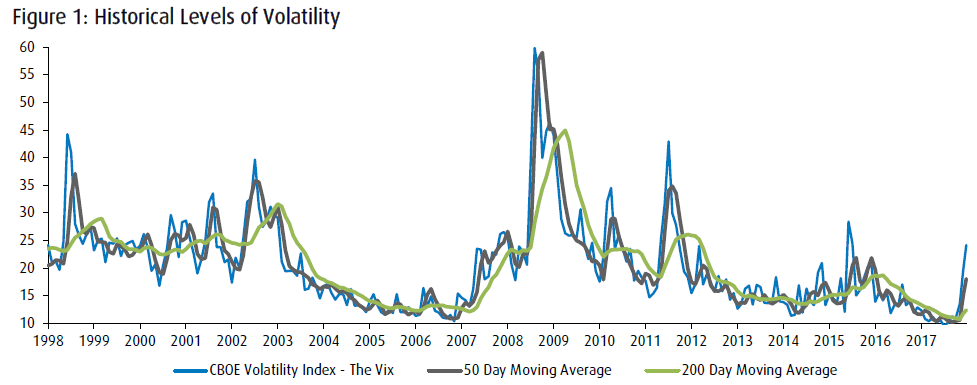

-March 29, 2018 Market Update. The U.S. equity markets have been unruly, largely dragged down by Tech darlings like Facebook (FB), Twitter (TWTR), Netflix (NTFX), Alphabet (GOOGL), among other past market leaders – which has rippled into other sectors and retested the market support set with February’s low when the S&P 500 hit 2,581. However, even with the spike in volatility this year the overall stock volatility is not particularly elevated relative to the last 20 years (see chart below). Indeed, recent market action is not “abnormal” over a historical longer-term perspective. The fact is any sharp market movement appears overblown relative to last year, when volatility declined to historically low levels. During these times of uncertainty investors need to have a broader perspective that strong corporate earnings are intact, GDP is growing at a healthy +2.7%, unemployment remains at a historical low and financial institutions remain sound. The synchronized global economies continue to recover while the credit market also remains a source of liquidity; the bond market does not see a major problem looming. Finally, bear markets are almost always associated with recessions. Warren Buffett (the sage of Omaha) has said, “the stock market is a device for transferring money from the impatient to the patient.” At this stage it is important to also remind investors that portfolios should embrace the diverse breadth of the investment universe – having access to an exceptionally diverse pool of investments enhances the potential for both returns and risk diversification.

-March 23, 2018 Weekly Market Update. The equity markets took a dive on the heel of proposed Trump Administration actions that could spur trade wars (new round of $60 billion tariffs on China-based exports), Facebook data breach that rippled through other social media stocks due to new regulatory concerns, a revolving door of top WH official turnover and uncertainty over the Fed Reserve in managing a growth economy with rising rates. More specifically related to the Fed, there is uneasiness in the capital markets over whether the Fed will become hawkish and hit the economic breaks too many times with Fed hikes and how these rate actions may become an albatross on the current 2.7% GDP growth trajectory. With the equity markets yet to find ground after the early February correction, these negative developments rippled through the major U.S. stock indices with the S&P 500 -5.93%, Dow -3.68% and Nasdaq -6.54% for the week. We can't emphasize enough the benefits of a diverse multi-asset portfolio during these periods of market stress. For example, our client portfolio downside correlation to these events remain in the 0.40-0.60 range - and for those more recent clients in which we have had high cash balances due to elevated valuations - we have now been able to find favorable pricing entry points into high conviction, quality securities.

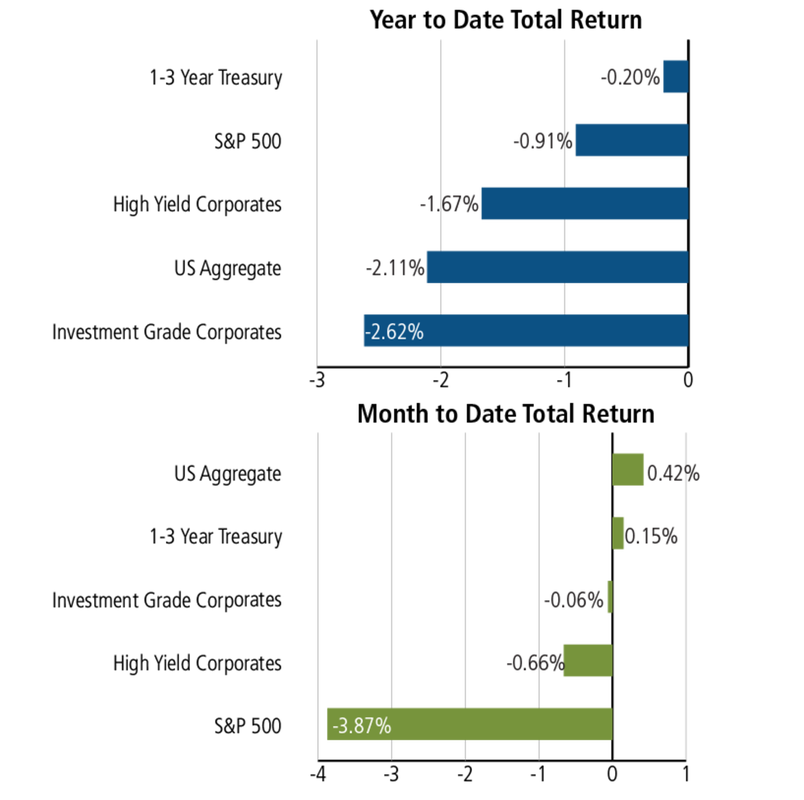

-March 22, 2018 Market Update. While the U.S equity markets continue to show volatility that are not uncharacteristic for a market seeking stability after the correction in early Feb, Trump’s trade war rattling has shown itself to be an ongoing troubling market force. This wall of worry was exacerbated by Trump’s lead personal attorney resigning and reverberations from yesterday’s Facebook data breach. The result of these factors was the S&P 500 -2.52%, Dow -2.93% and Nasdaq -2.43% (YTD the S&P is -0.68%, Dow -2.56% and Nasdaq +3.81%). As advisors, we used this market upheaval period to put some cash to work in high conviction assets deemed overly-punished by widespread capitulation.

-Market 21, 2018 Market Update. The Federal Reserve moved rates +0.25% today to 1.75%, which was in line with expectations. Powell, the Fed Chair, also appeared less hawkish with an indication that the expected three rate increase for the year remains unchanged; though it was indicated that the Fed would remain open to sharper increases should the economy overheat. The Fed also increased the GDP growth rate for the year to 2.7% from 2.4%. The S&P 500 and Dow industrials both slid -0.18%, while the Nasdaq fell 0.26% for the day. The average 30-year fixed-rate is now about 4.5%, up from 4.15% on Jan. 1st and significantly higher than the record low of 3.5% back in December of 2012.

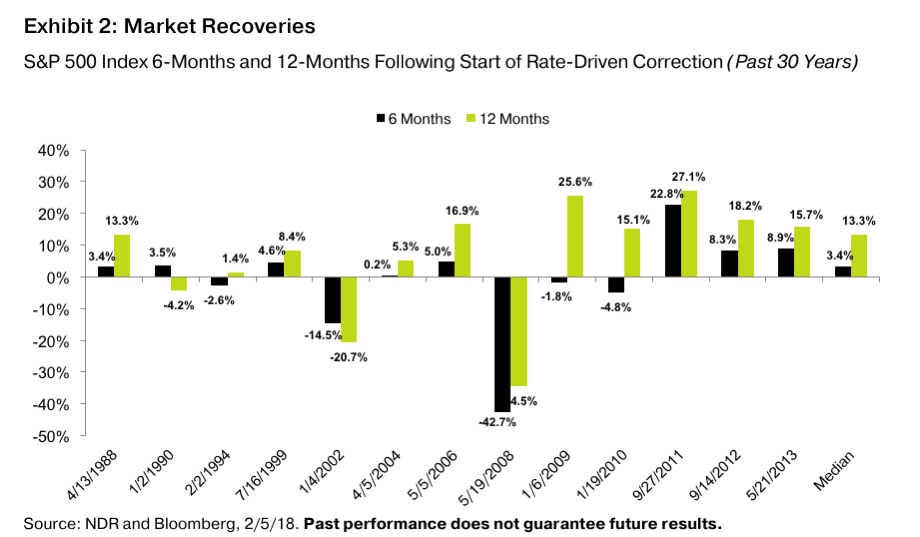

-March 19, 2018 Market Update. Over the past five (5) trading days, the S&P 500 has given back -2.48% and the Nasdaq -3.22%. During periods of volatility it is a great time to reevaluate investor risk aptitude and potentially reallocate investment holdings. However, it is also paramount that investors keep their long-term investment objectives in place and not make emotional decisions. As investment advisors we consider short-term price volatility as an opportunity and high price valuations as risk. We also emphasize that the understanding of risks embedded in a portfolio is central to providing value to our clients. We subscribe to managing dynamic factor exposures while still delivering broadly diversified, economically representative portfolios. We think of investing in terms of probabilities instead of binary outcomes and therefore we apply a selective multi-asset return approach of diversity for risk management. We also continue to educate our clients on investing and think it is important to share valuable historical perspectives on periods characterized by market stress and volatility. For example, from the beginning of the equity market correction decline, of which the -10% was reached back on February 8th of this year, the median return of the S&P 500 Index has been +3.4% after a period of six-months. However, the more telling fact is that 12 months from the beginning of the equity market correction decline the median return of the S&P 500 Index has been +13.3%. Also, these corrections were driven by changes in rates, causing overall market jitters over interest rates. (Refer to Exhibit 2, below)

-Market 21, 2018 Market Update. The Federal Reserve moved rates +0.25% today to 1.75%, which was in line with expectations. Powell, the Fed Chair, also appeared less hawkish with an indication that the expected three rate increase for the year remains unchanged; though it was indicated that the Fed would remain open to sharper increases should the economy overheat. The Fed also increased the GDP growth rate for the year to 2.7% from 2.4%. The S&P 500 and Dow industrials both slid -0.18%, while the Nasdaq fell 0.26% for the day. The average 30-year fixed-rate is now about 4.5%, up from 4.15% on Jan. 1st and significantly higher than the record low of 3.5% back in December of 2012.

-March 19, 2018 Market Update. Over the past five (5) trading days, the S&P 500 has given back -2.48% and the Nasdaq -3.22%. During periods of volatility it is a great time to reevaluate investor risk aptitude and potentially reallocate investment holdings. However, it is also paramount that investors keep their long-term investment objectives in place and not make emotional decisions. As investment advisors we consider short-term price volatility as an opportunity and high price valuations as risk. We also emphasize that the understanding of risks embedded in a portfolio is central to providing value to our clients. We subscribe to managing dynamic factor exposures while still delivering broadly diversified, economically representative portfolios. We think of investing in terms of probabilities instead of binary outcomes and therefore we apply a selective multi-asset return approach of diversity for risk management. We also continue to educate our clients on investing and think it is important to share valuable historical perspectives on periods characterized by market stress and volatility. For example, from the beginning of the equity market correction decline, of which the -10% was reached back on February 8th of this year, the median return of the S&P 500 Index has been +3.4% after a period of six-months. However, the more telling fact is that 12 months from the beginning of the equity market correction decline the median return of the S&P 500 Index has been +13.3%. Also, these corrections were driven by changes in rates, causing overall market jitters over interest rates. (Refer to Exhibit 2, below)

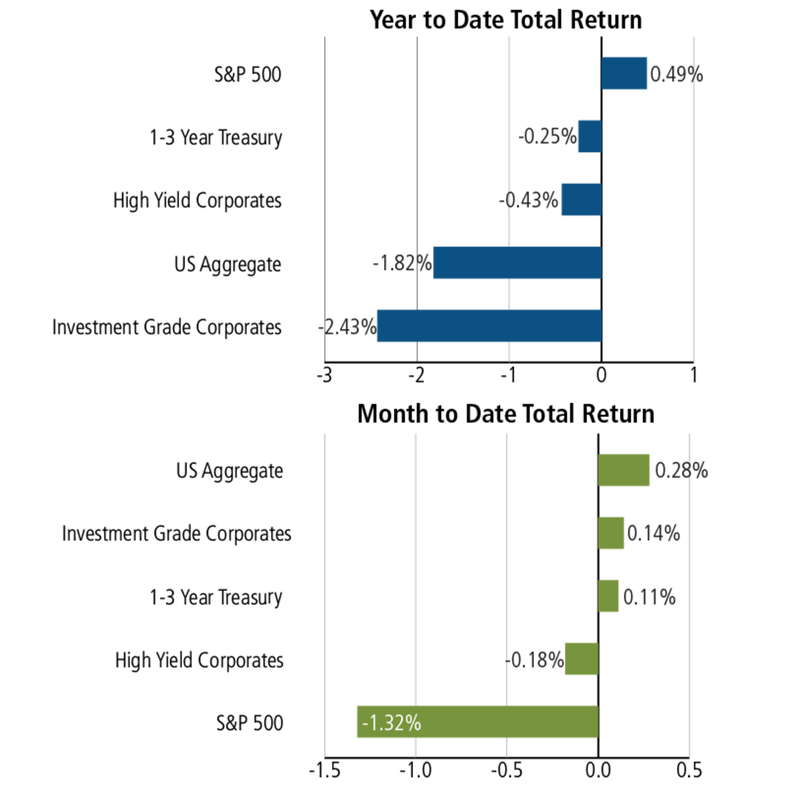

-March 16, 2018 Weekly Market Update. Equity market volatility remained elevated while U.S. equity indexes lost ground for the week: S&P 500 -1.20%, Dow Jones -1.51% and Nasdaq -1.04%. Placing the ongoing market volatility into perspective, the S&P 500 has moved by more than 1% in nine (9) of the 11 weeks this year, compared with 13 such weeks for the entire year of 2017. The negative market tone was largely driven by ongoing political uncertainty of top WH job shifts including the Secretary of State and Trump’s top economic advisor. Compounding this internal upheaval was a report that surfaced suggesting the WH plans to announce a new round of tariffs aimed at up to $60 billion in annual Chinese imports (e.g., electronics, telecommunications equipment, furniture & toys) in retaliation for intellectual property theft. After Gary Cohn’s resigned from the role WH Chief Economic Advisor last week, President Trump tapped Larry Kudlow as director of the National Economic Council. Mr. Kudlow’s initial economic remarks as the new incoming advisor was a call for “phase two” of tax reform, which would make individual tax cuts permanent and lower the capital gains tax rate.

-Montecito Capital Management Group and its Founder, Kipley J. Lytel, CFA is honored to have again been ranked in the Top 20 Financial Advisors List for 2018, particularly given the depth of 898 peer advisory firms considered. According to Managing Wealth Advisor, Lytel “We continue to be impressed with the rigorous selection process employed by Expertise, which includes a three-step process that scored financial advisors on more than 25 variables across five categories, and analyzed the results to give you a hand-picked list of the best regional financial advisors in California.” Lytel also expressed that “It is rewarding to be recognized for our outstanding investment advisory services by a neutral, third-party advisor ranking entity. Indeed, the five determining factors of Reputation, Credibility, Experience, Availability & Professionalism are a ‘Best of Breed’ hallmark for California-based wealth management practices.”

-This fact about female executives speaks for itself: "Over the past seven years, S&P 500 companies where at least 25% of executives were female generated higher one-year returns on equity than the overall index, on a median basis, according to data compiled by the BofA." Moreover, according to McKinsey study: "Companies in the top quartile for gender diversity were 15% more likely to see their operating income surpass the industry median."

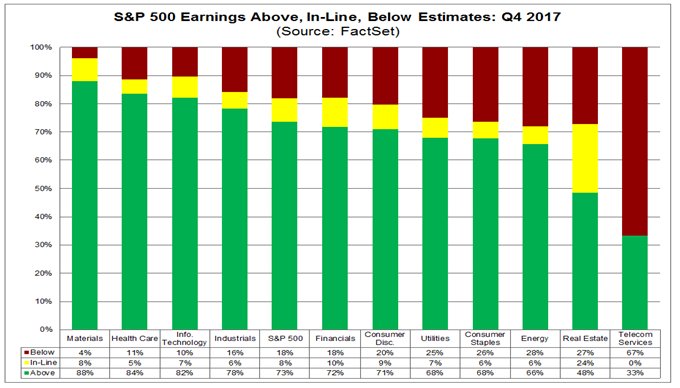

-March 9, 2018 Weekly Market Update. The equity markets traded down most of the week on fears of a trade war, but quickly rebounded on news that steel and aluminum tariffs would exclude imports from Canada and Mexico. The stock market's late week recovery was also aided by strong economic data punctuated by an outstanding employment report, with a whopping 313,000 new jobs reported in February. For the week, the S&P 500 returned +3.59%, the Dow Jones gained +3.34% and the Nasdaq surged +4.17%. On the earnings front, 73% of the S&P 500 ($SPX) companies beat EPS estimates for Q4, a figure that is well above the 5-year average of 69%. Since the US trade deficit continues to expand, it is our view that this provides a good pulse on the health of our U.S. economy where robust domestic demand continues to drive import activity. It’s when the trade deficit shrinks, well, that is when investors should look deeper in the trade numbers to determine if it is slowing demand or currency exchange headwinds.

-This fact about female executives speaks for itself: "Over the past seven years, S&P 500 companies where at least 25% of executives were female generated higher one-year returns on equity than the overall index, on a median basis, according to data compiled by the BofA." Moreover, according to McKinsey study: "Companies in the top quartile for gender diversity were 15% more likely to see their operating income surpass the industry median."

-March 9, 2018 Weekly Market Update. The equity markets traded down most of the week on fears of a trade war, but quickly rebounded on news that steel and aluminum tariffs would exclude imports from Canada and Mexico. The stock market's late week recovery was also aided by strong economic data punctuated by an outstanding employment report, with a whopping 313,000 new jobs reported in February. For the week, the S&P 500 returned +3.59%, the Dow Jones gained +3.34% and the Nasdaq surged +4.17%. On the earnings front, 73% of the S&P 500 ($SPX) companies beat EPS estimates for Q4, a figure that is well above the 5-year average of 69%. Since the US trade deficit continues to expand, it is our view that this provides a good pulse on the health of our U.S. economy where robust domestic demand continues to drive import activity. It’s when the trade deficit shrinks, well, that is when investors should look deeper in the trade numbers to determine if it is slowing demand or currency exchange headwinds.

-Fair trade is challenging with China and that is why a blunt object like a tariff is a crude tool for a complex problem. China is a master manipulator - case in point, as part of the membership into the World Trade Organization (WTO) China was required to reform thousands of laws, yet China failed to deliver the big items like opening telecom mkt, reform state-owned enterprises, halt manipulation of technology standards, etc. Adding salt into the wound is that since China is now part of the WTO they have abused that membership to win regulatory sanctions against US companies like Qualcomm and pushing agendas to force US tech companies to turn over user data and intellectual properties to their gov't. The US Information Technology & Innovation Foundation says our country is not pursuing "constructive confrontation" on these matters, and due to this neglect, US companies are suffering. The upside is China's currency (yuan) is currently free floating now and has surged against the USD which will be hurting their export competitiveness.

-March 3, 2018 Trump Tariff Viewpoint: Going back to 1776 Adam Smith, tariffs have had a disruption effect that hurts the many at the benefit of the few (steel industry). George Bush tried some steel tariffs briefly and while it effectuated a brief industry boost, it still didn’t work out for the steel workers in the long-run. It is not about why can others get away with it. The U.S. is the largest economy in the world and therefore there will be far more significant negative ramifications. The bigger issue is other countries will retaliate with tariffs and this will create both pricing and industry disruption when for the first time in over a decade the entire world is finally growing GDP in tandem (general economic health worldwide). Even China has been moving in the right direction - in 2015 China reduced many import tax rates for clothing, footwear, skincare products, diapers and other consumer goods to boost domestic consumption. The average reduction is more than 50 percent. The odds are that many products will be going higher for our US consumers (steel based-products like autos-airplanes-bikes, blue jeans, even beer!) and Europe has already responded with a proposed tariff against Harley Davidson, Electrolux not making the $250M cooking factory in Tennessee, etc. None of this is good and clearly is at odds with prevailing economic theory, including painful historical lessons going back to the Great Depression (Smoot-Hawley Tariff). Tariffs derail free market competition and this competition enables the consumer to reap the lowest price. Now the price of the good with the tariff has increased, the consumer is forced to either buy less of this good or less of some other good. The price increase can be considered a reduction in consumer income. Since consumers are purchasing less, domestic producers in other industries are selling less, engendering a decline in the economy (if trade ware escalates to other industries). Incidentally, our firm is on record as early as Nov 9, 2016, in a Wealth Management Magazine article where firm founder, Kipley Lytel CFA expressed concern over the potential for Trump protectionist policies engendering a trade war:

http://www.wealthmanagement.com/industry/many-advisors-smile-trump-s-victory

-March 2, 2018 Weekly Market Roundup. Volatility returned to the equity markets this week as stocks sold off on announced tariffs on steel (25%) and aluminum imports (10%), raising fears of a trade war. All U.S. equity market indices reported losses for the first week of March with the S&P 500 -1.98%, Dow Jones -2.97% and Nasdaq -1.12%. Meanwhile, the (CBOE VIX) jumped 19% to 19.59; despite the spike in VIX, volatility remains down more than 50% from its intraday peak last month. The capital markets are also still processing the upbeat Fed Chair (Powell) outlook that indicated a possible fourth rate hike this year, up from the three originally planned. It is our view that volatility typically continues for a short period after a market correction (-10%) and history tells us that this is not an uncommon occurrence in long-running bull markets. In fact, a recent Guggenheim study revealed “The majority of declines fall within the 5-10 percent range with an average recovery time of approximately one month, while declines between 10-20 percent have an average recovery period of approximately three months.”

-March 3, 2018 Trump Tariff Viewpoint: Going back to 1776 Adam Smith, tariffs have had a disruption effect that hurts the many at the benefit of the few (steel industry). George Bush tried some steel tariffs briefly and while it effectuated a brief industry boost, it still didn’t work out for the steel workers in the long-run. It is not about why can others get away with it. The U.S. is the largest economy in the world and therefore there will be far more significant negative ramifications. The bigger issue is other countries will retaliate with tariffs and this will create both pricing and industry disruption when for the first time in over a decade the entire world is finally growing GDP in tandem (general economic health worldwide). Even China has been moving in the right direction - in 2015 China reduced many import tax rates for clothing, footwear, skincare products, diapers and other consumer goods to boost domestic consumption. The average reduction is more than 50 percent. The odds are that many products will be going higher for our US consumers (steel based-products like autos-airplanes-bikes, blue jeans, even beer!) and Europe has already responded with a proposed tariff against Harley Davidson, Electrolux not making the $250M cooking factory in Tennessee, etc. None of this is good and clearly is at odds with prevailing economic theory, including painful historical lessons going back to the Great Depression (Smoot-Hawley Tariff). Tariffs derail free market competition and this competition enables the consumer to reap the lowest price. Now the price of the good with the tariff has increased, the consumer is forced to either buy less of this good or less of some other good. The price increase can be considered a reduction in consumer income. Since consumers are purchasing less, domestic producers in other industries are selling less, engendering a decline in the economy (if trade ware escalates to other industries). Incidentally, our firm is on record as early as Nov 9, 2016, in a Wealth Management Magazine article where firm founder, Kipley Lytel CFA expressed concern over the potential for Trump protectionist policies engendering a trade war:

http://www.wealthmanagement.com/industry/many-advisors-smile-trump-s-victory

-March 2, 2018 Weekly Market Roundup. Volatility returned to the equity markets this week as stocks sold off on announced tariffs on steel (25%) and aluminum imports (10%), raising fears of a trade war. All U.S. equity market indices reported losses for the first week of March with the S&P 500 -1.98%, Dow Jones -2.97% and Nasdaq -1.12%. Meanwhile, the (CBOE VIX) jumped 19% to 19.59; despite the spike in VIX, volatility remains down more than 50% from its intraday peak last month. The capital markets are also still processing the upbeat Fed Chair (Powell) outlook that indicated a possible fourth rate hike this year, up from the three originally planned. It is our view that volatility typically continues for a short period after a market correction (-10%) and history tells us that this is not an uncommon occurrence in long-running bull markets. In fact, a recent Guggenheim study revealed “The majority of declines fall within the 5-10 percent range with an average recovery time of approximately one month, while declines between 10-20 percent have an average recovery period of approximately three months.”

-February 28, 2018 Monthly Market Roundup. February marked the worst month in over two years for the U.S. stock market on the heels of the -3.9% drop in the S&P 500. The month also concluded a 10-percent correction for the stock market; fortunately, strong earnings drove a partial rebound that made the monthly losses less precipitous. The S&P 500 is now down about 5.6 percent from its Jan. 26 record high. However, not only has the stock market correction relieved the market’s extreme overbought and low volatility conditions, the market showed a relatively strong recovery for the month until Fed Chair Powel hinted that the economic environment might justify four rate increases for the year (vs. the previously anticipated 3 rate hikes). Hence, the resurfacing threat of higher inflation and interest rates - which also was largely responsible for the earlier -10% correction - remained a worrisome overhang on the markets. It is our view that the 10-year treasury yield would need to exceed 4.75% before any recessionary impact on stocks (10-yr yield is currently 3.85%). We also foresee continued flattening of the yield curve and higher rates improving the outlook for short versus longer-term bond maturities. The good news: About 76% of the S&P 500 companies that have reported earnings have topped profit estimates - that is above the average 72% average for the past four quarters. Also, for 2018, S&P 500 earnings estimates have increased by $11.21 per share from $146.26 to $157.47. That’s a 7.7% increase. Overall, expectations are that corporate profits will keep rising and the global economy should keep strengthening.