-September 30, 2017 Weekly Market Roundup. All US equity indexes rallied for the week, led by small caps and both the energy and technology sector. The S&P 500 gained +0.72%, the Nasdaq jumped +1.07% and the Dow Jones finished +25%. U.S. small-cap stocks are more sensitive to changes in the domestic tax code and have therefore rebounded on the proposed government tax plan. Meanwhile, energy has been oversold and is also being buoyed by the incremental oil recovery since June. In turn, bonds largely lost ground across the board for the week with Barclay’s US Aggregate Bond index and Barclay’s US Government Bond Index down -0.10% and -0.27%, respectfully.

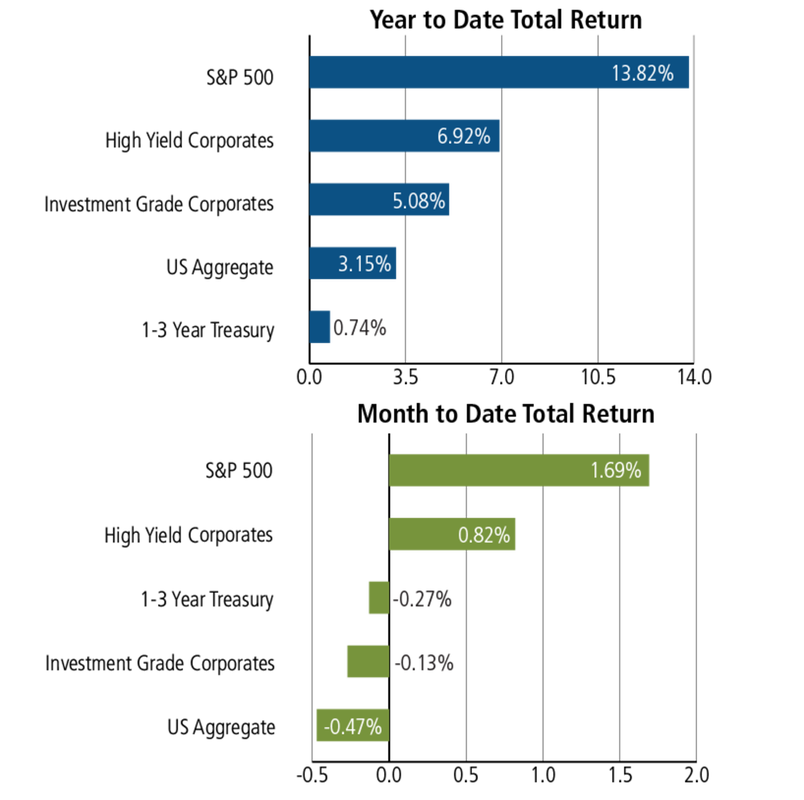

With regard to the multi-asset returns through mid-week, see the follow chart below:

With regard to the multi-asset returns through mid-week, see the follow chart below:

-September 15, 2017 Weekly Market Roundup. The S&P 500 and the Dow finished at record highs with the S&P advancing +1.6% and the Dow rising +2.2%; Nasdaq missed its all-time high after climbing +1.4%. Leading the charge was the Energy sector that finished up +3.9% in tandem with rising fuel prices on the heal of disruptions from the recent Hurricanes.

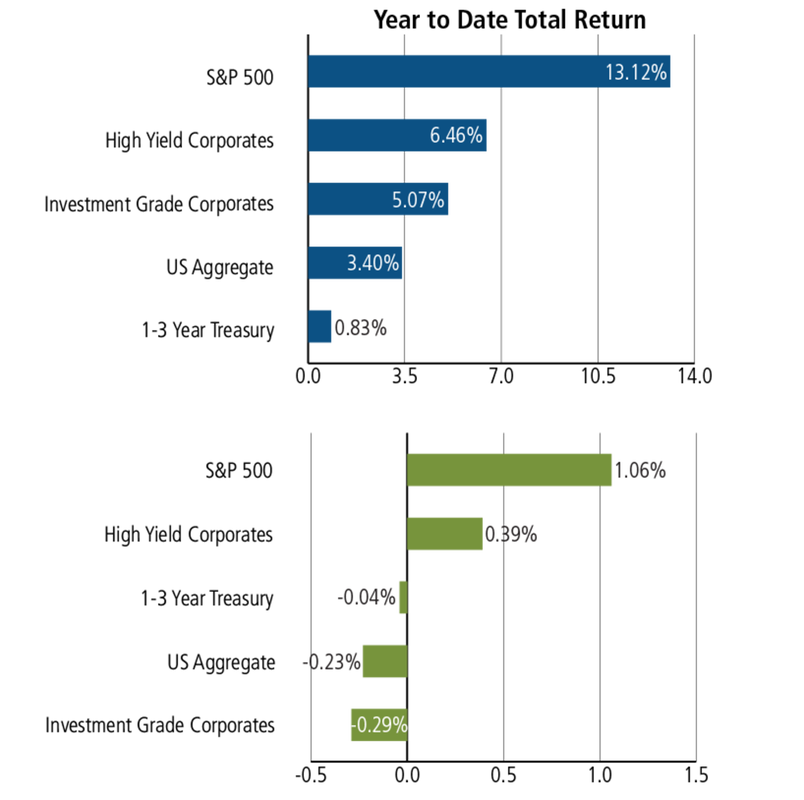

Below are index returns as of the market close for mid-week:

Below are index returns as of the market close for mid-week:

-September 8, 2017 Weekly Market Roundup. Equity markets exhibited weakness during the truncated trading week (holiday) with the S&P 500 slipping -0.58%, the Nasdaq dropping -1.17% and the Dow Jones declining -0.82%. The capital markets have become rattled by hurricanes, legislative surprises and aggravated tensions with North Korea. Another broader concern is the economic impact of several regions in the US being devastated by hurricanes; already, initial claims for unemployment insurance, a leading indicator of economic weakness, increased +53,000 to 298,000 for the week ending September 2, 2017.

-September 1, 2017 Weekly Market Roundup. Equity markets bounced back for the week on several economic upside developments including 2Q GDP revised upward to 3.0% growth, wholesale inventories +0.4%, August employment change +237k (vs. +180k est), personal income +0.4% (vs. 0.3% est) and ISM manufacturing (58.8 vs 56.8 est). Further, the capital markets positively responded to Trump’s tax reform push highlighting simplified tax codes, lower taxes and repatriating offshore corporate cash hoards. For the week, the S&P 500 gained +1.43%, the Dow Jones +0.88% and the Nasdaq ended +2.71%.

-If history is any guide, September might be a tough market for stocks; it is historically the worst month for equities and the only one with statistically significant negative returns. Stocks have already receded -3% this summer and in our opinion, a bit more correction and consolidation is due.

-September 1, 2017 Weekly Market Roundup. Equity markets bounced back for the week on several economic upside developments including 2Q GDP revised upward to 3.0% growth, wholesale inventories +0.4%, August employment change +237k (vs. +180k est), personal income +0.4% (vs. 0.3% est) and ISM manufacturing (58.8 vs 56.8 est). Further, the capital markets positively responded to Trump’s tax reform push highlighting simplified tax codes, lower taxes and repatriating offshore corporate cash hoards. For the week, the S&P 500 gained +1.43%, the Dow Jones +0.88% and the Nasdaq ended +2.71%.

-If history is any guide, September might be a tough market for stocks; it is historically the worst month for equities and the only one with statistically significant negative returns. Stocks have already receded -3% this summer and in our opinion, a bit more correction and consolidation is due.