-February 22, 2019 Weekly Capital Market Update. Equity markets edged higher on China-U.S. trade prospects with the Trump-XI meet and Fed comments expressing continued uncertainty over future rate hikes: S&P 500 +0.62%, Dow Jones +0.57% and Nasdaq +0.74% on the week. There reportedly was a Memorandum of Understanding on some key China-U.S. trade items and Trump indicated that he may extend the trade deal deadline should there be some earnest progress. The Dow Jones and S&P 500 are now riding a nine-week winning streak - returns for year have both are up over 11% marking the best start since 1987 and 1991. Clearly stocks are "overbought" now, but they can stay that way for a while. However, historically when these equity indices move in sync through Feb, the trend often continues through year-end – at least 60% of the time. The current underbelly of this market recovery is the Fed’s stance toward accommodation, constructive progress on a China trade deal (partly motivated by China taking it in the shorts with its economy) and the overall economic engine. As for the latter category, the current trends are mixed: homes sales/construction down, service industry up, retail sales down (though Walmart knocked it out of the park on earnings), employment steady and at decades’ low for unemployed, Philly Fed dropping to 31-month low of 4.1 (measures changes in business growth), etc. Consensus analyst estimates for 2019 are far more tepid than past years with earnings & sales growth of +4.5% and 4.9%, respectively. We didn’t take our risk allocation down much this past week but will continue to look for days of meaningful market strength to deflate risk exposure in client portfolios.

-February 15, 2019 Weekly Capital Market Update. All U.S. equity markets rallied on the week marked by elevated positive expectations with U.S.-China trade talks and the avoidance of another government shutdown: S&P 500 gained +2.5%, Dow Jones +3.09% and Nasdaq +2.53%. The markets were also aided by Fed commentary reinforcing their intention to maintain liquidity near current levels. The market is also feeding off old economic news as related to fourth quarter 2018 earnings where the S&P 500 ($SPX) is reporting earnings growth of 13.1% for Q4 2018, which would be the 5th straight quarter of double-digit earnings growth. The S&P 500 has recovered from its lows and now site about 6% off the all-time-highs. However, our investment approach has used this impressive Jan-Feb rally to reduce market exposure; we will continue to feather down equity weightings should the market march upward. We believe the market valuations have gotten ahead of themselves (doesn’t mean it won’t go higher) given most of the good news is backward looking. In fact, the S&P 500 EPS estimate for Q119 has declined by -4.8% over the past 12 months and by -5.4% since Dec. 31 and the Conference Board’s Measure of CEO Confidence plunged -13 points to 42 in last year’s 4th quarter; this is the 3rd consecutive drop & now below key recession level of 43. Forward-looking data considerations should take consideration of that fact that more than half of the banks that reported earnings noted tighter standards due to an “uncertain economic outlook” and weak demand for loans. Therefore, we reiterate our stance of keeping powder dry for any market pullback, while also lower risk by investing in this (now) higher yielding fixed-income environment. Another cloud is uncertainties overseas: Brexit (U.K. economy 6-yr low), Italy’s slumbering economy & questionable leadership, economic unrest in France over taxes, etc.

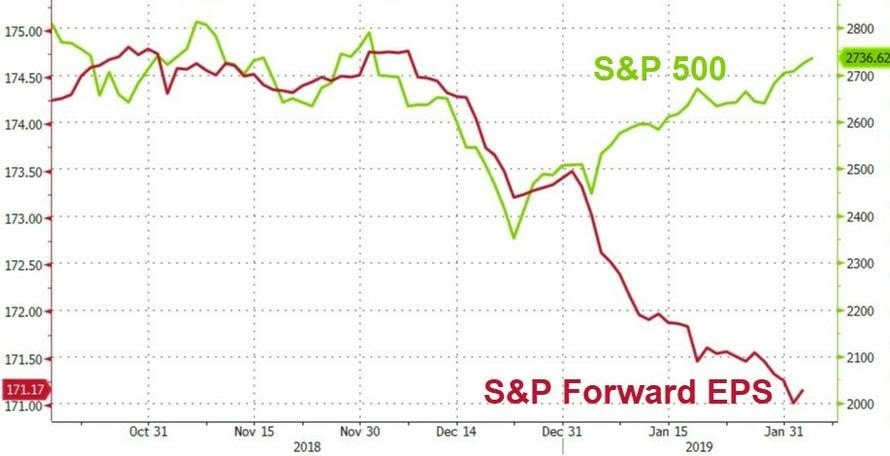

-February 6, 2019 Weekly Capital Market Update. The major equity indices nudged forward with a week marked by increased volatility: S&P 500® Index +0.05%, Nasdaq gained +0.55%, and Dow Jones Industrial Average +0.17%. The markets started the week on a positive trend then were rattled by Brexit and trade concerns. For example, President Trump said that he would not meet with China's President Xi before a March 1st deadline set by the two countries to achieve a trade deal. The remarks dampened growing optimism for a trade deal in the short term and weighed on stocks. However, fundamentals seem intact with earnings results from 66% of companies in the S&P 500 showing growth rate of 13.3%; on pace for a fifth consecutive quarter of double-digit growth. Market focus will continue on earnings reports and the expected Congressional action to avoid another government shutdown which could take effect on February 15th. The S&P now sits 7+% off the all-time highs, and investors are struggling to determine whether the markets can complete the "V" type of recovery from December lows. We reiterate our approach of incrementally phasing down risk during periods of market strength – lowering equity exposure through 2019. The rationale is we expect elevated economic headwinds in 2020 and the market prognosticator will react to any negative events months ahead of the hard data. Case in point, FactSet has revised their S&P 500 2019 year earnings and revenue forecast to +5%, which is far below past periods of double digit growth and certainly inconsistent with expanding equity valuation multiples [see chart below]. From the technical standpoint, sentiment remains positive as buyers have stepped in toward the end of the market trading day to help buy up the dips. Final thought is the market has built in expectations for a high level of corporate stock buybacks in 2019 – probably at least over $600 billion – but Congress has recently indicated intervention to curb this activity. We contend that buybacks are indeed often ineffective use of corporate piggybanks (should go to dividends and capital expenditures), but at the same time this mechanism has been supportive of equity market valuations and should it taper, then equity markets will lose a powerful buyer constituent of stocks.

-February 15, 2019 Weekly Capital Market Update. All U.S. equity markets rallied on the week marked by elevated positive expectations with U.S.-China trade talks and the avoidance of another government shutdown: S&P 500 gained +2.5%, Dow Jones +3.09% and Nasdaq +2.53%. The markets were also aided by Fed commentary reinforcing their intention to maintain liquidity near current levels. The market is also feeding off old economic news as related to fourth quarter 2018 earnings where the S&P 500 ($SPX) is reporting earnings growth of 13.1% for Q4 2018, which would be the 5th straight quarter of double-digit earnings growth. The S&P 500 has recovered from its lows and now site about 6% off the all-time-highs. However, our investment approach has used this impressive Jan-Feb rally to reduce market exposure; we will continue to feather down equity weightings should the market march upward. We believe the market valuations have gotten ahead of themselves (doesn’t mean it won’t go higher) given most of the good news is backward looking. In fact, the S&P 500 EPS estimate for Q119 has declined by -4.8% over the past 12 months and by -5.4% since Dec. 31 and the Conference Board’s Measure of CEO Confidence plunged -13 points to 42 in last year’s 4th quarter; this is the 3rd consecutive drop & now below key recession level of 43. Forward-looking data considerations should take consideration of that fact that more than half of the banks that reported earnings noted tighter standards due to an “uncertain economic outlook” and weak demand for loans. Therefore, we reiterate our stance of keeping powder dry for any market pullback, while also lower risk by investing in this (now) higher yielding fixed-income environment. Another cloud is uncertainties overseas: Brexit (U.K. economy 6-yr low), Italy’s slumbering economy & questionable leadership, economic unrest in France over taxes, etc.

-February 6, 2019 Weekly Capital Market Update. The major equity indices nudged forward with a week marked by increased volatility: S&P 500® Index +0.05%, Nasdaq gained +0.55%, and Dow Jones Industrial Average +0.17%. The markets started the week on a positive trend then were rattled by Brexit and trade concerns. For example, President Trump said that he would not meet with China's President Xi before a March 1st deadline set by the two countries to achieve a trade deal. The remarks dampened growing optimism for a trade deal in the short term and weighed on stocks. However, fundamentals seem intact with earnings results from 66% of companies in the S&P 500 showing growth rate of 13.3%; on pace for a fifth consecutive quarter of double-digit growth. Market focus will continue on earnings reports and the expected Congressional action to avoid another government shutdown which could take effect on February 15th. The S&P now sits 7+% off the all-time highs, and investors are struggling to determine whether the markets can complete the "V" type of recovery from December lows. We reiterate our approach of incrementally phasing down risk during periods of market strength – lowering equity exposure through 2019. The rationale is we expect elevated economic headwinds in 2020 and the market prognosticator will react to any negative events months ahead of the hard data. Case in point, FactSet has revised their S&P 500 2019 year earnings and revenue forecast to +5%, which is far below past periods of double digit growth and certainly inconsistent with expanding equity valuation multiples [see chart below]. From the technical standpoint, sentiment remains positive as buyers have stepped in toward the end of the market trading day to help buy up the dips. Final thought is the market has built in expectations for a high level of corporate stock buybacks in 2019 – probably at least over $600 billion – but Congress has recently indicated intervention to curb this activity. We contend that buybacks are indeed often ineffective use of corporate piggybanks (should go to dividends and capital expenditures), but at the same time this mechanism has been supportive of equity market valuations and should it taper, then equity markets will lose a powerful buyer constituent of stocks.

-February 1, 2019 Weekly Capital Market Update. Stocks had the best January in 32 years with the S&P 500 rising nearly 8 percent in January. For the week the S&P 500® Index rose +1.57%, followed by the Nasdaq +1.38% and Dow Jones Industrial Average +1.32%. The capital markets were supported with relatively strong corporate earnings and the Fed indication that rates will remain stable with a patient approach; expect “ample” balance sheet accommodation. Also, U.S. Treasury Secretary Steven Mnuchin said that if China presents enough trade concessions to President Donald Trump, there is a chance that the administration may seek to lift all tariffs. Equities are likely to be buoyed by continued stock buybacks this year, according to JPMorgan. JPMorgan strategist Dubravko Lakos-Bujas says companies still have large amounts of cash overseas—funds that could be used for buybacks if sent home—and even better, stocks look much cheaper now. Lakos-Bujas wrote in a note on Friday. He predicts that S&P 500 companies will announce another $800 billion in buybacks this year. American companies sent home about $570 billion in foreign cash during the first three quarters last year as a result, but $1 trillion remains abroad and the repatriation will likely continue in 2019, writes Lakos-Bujas.