-January 27th, 2017 Weekly Market Roundup. The S&P 500 finished for a weekly gain of +1.0%, the NASDAQ was up +1.9% during the week and the Dow Jones Industrial Average Index closed above 20,000 for the first time ever this week. As of today (with 34% of the companies in the S&P 500 reporting actual results for Q4 2016), 65% of S&P 500 companies have beat the mean EPS estimate and 52% of S&P 500 companies have beat the mean sales estimate. For Q4 2016, the blended earnings growth rate for the S&P 500 is 4.2%. Also, the CBOE Volatility Index, the so-called “fear gauge,” hit a more than two-year low this week as signs of an improving global economy and expectations for business-friendly policies. The initial estimate of fourth quarter GDP showed the U.S. economy grew at a 1.9% rate, helped by strong consumer spending, a pickup in business investments, and a rebound in home construction. The pace exceeded weaker growth in the first half of 2016 but slowed considerably from third quarter’s 3.5% growth rate. The market probability for a rate hike at next week’s Fed meeting hovered at 22%.

-January 20th, 2017 Weekly Market Roundup. Equity markets finished slightly down for the week with the S&P 500 -0.2% decline, the Dow -0.3% and NASDAQ off -0.3%. Over the last month, the day-to-day changes in the S&P 500® Index have stayed within one percentage point while the Dow Jones Industrial Average has stalled just shy of reaching 20,000. Earnings for the fourth quarter kicked off with generally strong results for financial stocks that were the first to report. Of the 63 companies in the S&P 500® Index that have reported fourth quarter earnings results, 46% have exceeded sales estimates and 63% have exceeded earnings per share (EPS) estimates. Overall, analysts expect sales to rise 4.2%, to mark the Index’s fastest growth since the third quarter of 2014.

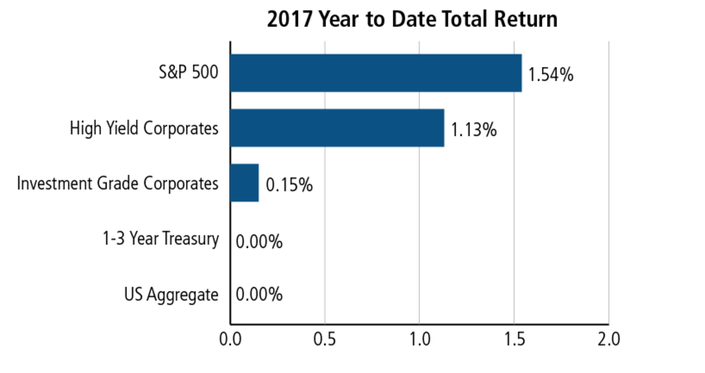

Total Returns by Asset Class (YTD Jan 20, 2017)

al equities. Since international markets peaked in 2007 right before a global financial meltdown, Morningstar data show that developed international stocks – as measured by the MSCI EAFE index – had lost a cumulative -6% through last week. At the same time, the MSCI Emerging Markets index had slid -16.6%.

-January 13th, 2017 Weekly Market Roundup. Markets shifted between modest gains and losses this week to close roughly unchanged. The upcoming fourth quarter corporate earnings reports should provide indications of near-term market direction, and more importantly, insight from management teams’ outlooks for the year. For example, a few large financial firms have reported fourth quarter results with favorable revenue & profit trends, including very positive remarks on the business prospects moving forward. Ahead of the reporting season, analysts are projecting the companies within the S&P 500 index to have revenue increases of +4.6%, along with improved earnings (+3.2%). The World Bank said this week it expects the world economy to expand +2.7% this year, on the heels of stabilizing and slightly rising commodity prices and fiscal stimulus in the US.

-The Conference Board’s Consumer Confidence Index climbed to 113.7 (1985=100) – the highest level since August 2001. It moved +4.3 points higher than November’s level, while beating the prior forecast of 109 (according to Bloomberg reports). Further, the Markets: Proportion of consumers expecting higher share prices in 2017 increased to 44.7% in December, the largest since January 2004.

-January 6th, 2017 Weekly Market Roundup. Equity markets welcomed the New Year with gains in all sectors as all major indices advanced. While the Dow fell just short of reaching 20,000, the S&P 500 closed at an all-time high on Friday. Driving much the rally has been the incoming Trump administration’s priorities including tax, health care, and regulatory reform as well as infrastructure spending. Also, helping equities march higher was the December jobs report, which showed that the economy added 156,000 jobs in December and average hourly earnings grew 2.9% over the past year.

Montecito Capital Management Group’s 2017 Market Outlook & Forecast:

As we enter 2017 we expect the current economic rebound to continue suggesting GDP growth will likely move toward the 2.7%-3.0% level by the end of the year based on less monetary stimulus, more fiscal stimulus, a reduction in the corporate tax rate and deregulation.

The S&P 500 equity index is currently trading at about a forward 2017 price-earnings ratio of 17x which is a rich value, but not as lofty as the 2000-2001 tech bubble (nor as cheap as 2009). Wall Street currently forecasts a +5.5% gain for the S&P 500 in 2017 (average of 15 firms) and sees the index reaching 2,363 by year end, from its 12/31/16 close of 2,239. We believe the market has the potential for +7.5% in 2017 given more indirect investment currents where lackluster bond downward pricing will likely engender an extended redistribution from bonds to equities. We also believe the S&P 500 returns will be front loaded, where the largest percentage of gains will be in the first half of 2017.

The incoming administration has promised a much more business-friendly atmosphere including lower taxes and less regulation. Trump has control over both houses of Congress. Also, in the years when that has occurred, equiteies have returned an average of +14% per annum. Having Congressional & Executive Branch control is historically rare for a Republican administration. Trump wants to cut the corporate tax rate, and congress is in agreement, making it likely to happen. According to Citi, if the rate was cut to 20%, it would add $12 to their top-down estimate of $130 for 2017 S&P 500 earnings per share (or about +10%,).

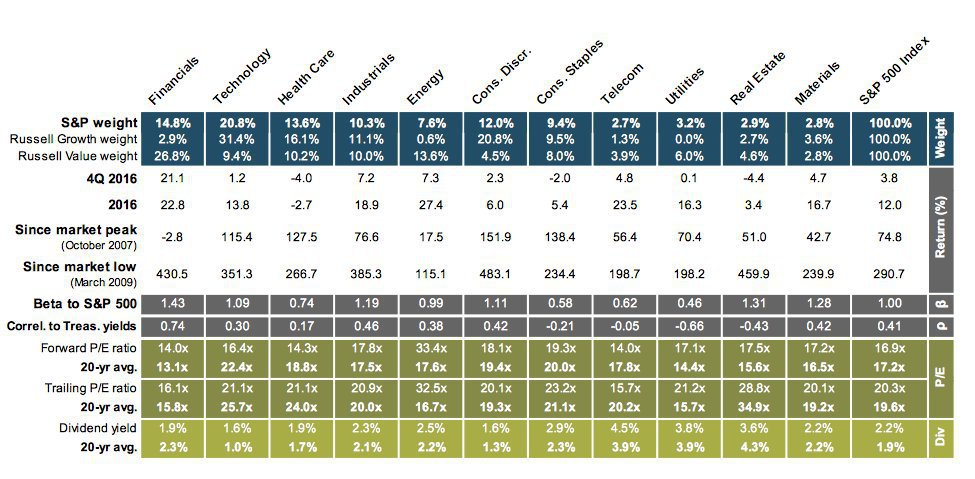

2016 Returns By Sector, Shows Clear Sector Winners, Losers & Benchwarmers: