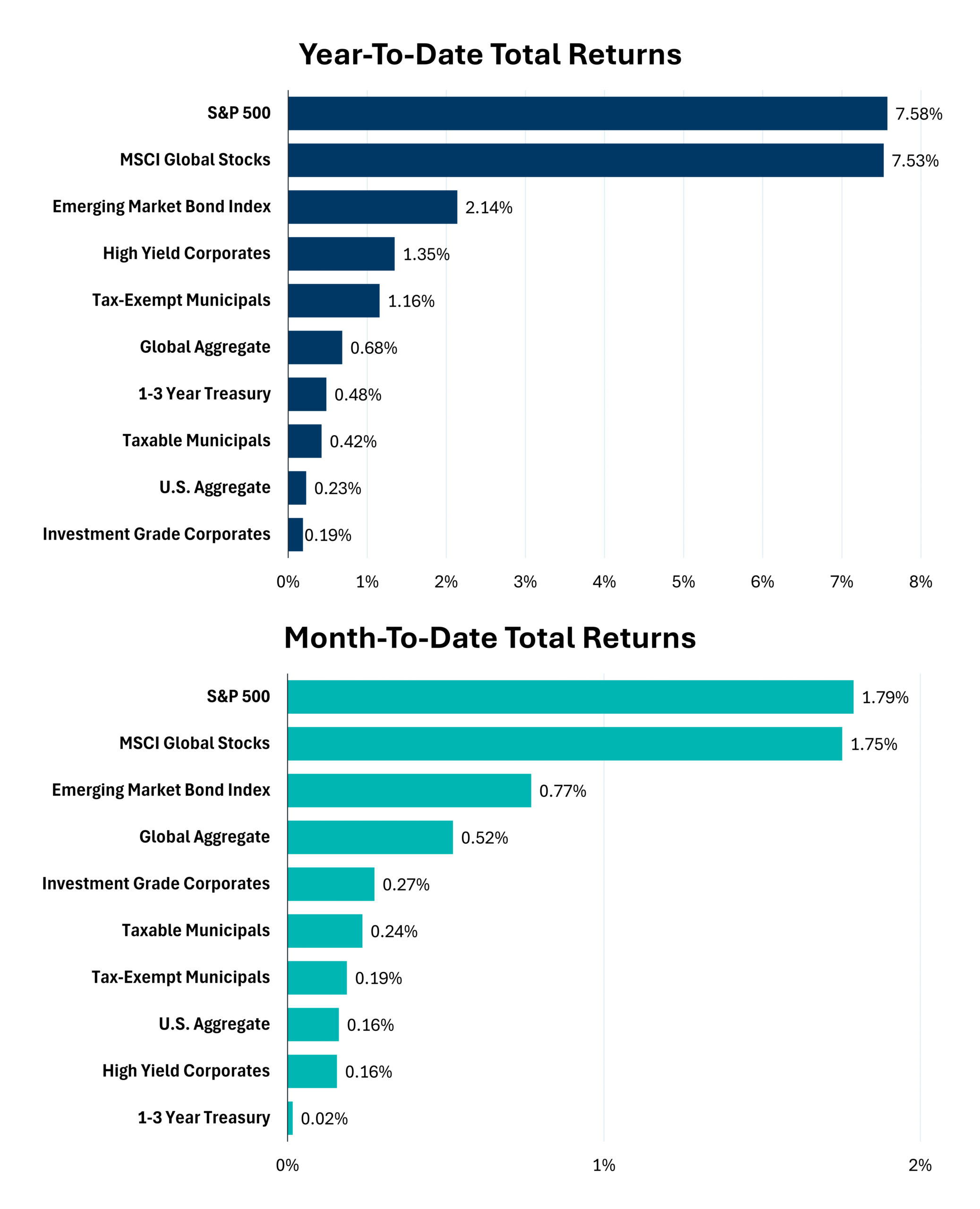

U.S. equities continued their strong advance this week, with technology stocks once again leading the rally and pushing the S&P 500 and Nasdaq to fresh record highs. For the week, the Nasdaq gained 4.5%, the S&P 500 rose 2.3%, and the Dow Jones Industrial Average added 0.2%.

Markets remained focused on several competing themes throughout the week, including resilient economic data, elevated oil prices tied to ongoing Middle East tensions, AI-driven earnings optimism, and renewed attention on U.S.-China trade discussions. Investor sentiment improved following stronger-than-expected employment data and continued strength in corporate earnings, particularly within large-cap technology and semiconductor companies.

Oil prices remained volatile as investors monitored developments surrounding Iran and the Strait of Hormuz, a critical global shipping route. While crude prices stayed elevated relative to recent months, easing fears of a broader supply disruption helped calm some of the market’s worst-case economic concerns later in the week.

Technology stocks again led the market higher, with AI-related infrastructure, semiconductor, and cloud companies driving much of the advance. Investors continued rewarding businesses benefiting from artificial intelligence spending, data-center expansion, and accelerating demand for computing power.

Economic data released this week showed U.S. nonfarm productivity increased 2.9% over the past year during the first quarter of 2026, continuing the stronger productivity trend seen since 2023. While many investors point to artificial intelligence adoption as the primary driver, the underlying explanation may be more nuanced. Productivity measures output per hour worked, and with relatively modest employment growth alongside still-resilient GDP growth, productivity readings naturally appear stronger. In addition, much of the recent economic expansion has been supported by significant AI-related capital investment that boosts output without requiring substantial increases in labor.

At the same time, several broader measures of economic efficiency suggest underlying productivity trends may not be accelerating as quickly as headline numbers imply. This reinforces the view that while AI-driven productivity gains remain promising over the long term, the full economic benefits are likely still in the early stages of development.

Looking ahead, markets will continue watching inflation data, Federal Reserve policy expectations, energy markets, and geopolitical developments for clues on whether the current market momentum can continue into the summer months.