Author: Montecito Capital Management

Liquidity is more than just cash in the bank; it is peace of mind. It is the safety net that allows you to weather unexpected emergencies without destabilizing your long-term investments. It is optionality — the freedom to make choices rather than be forced into them. Liquidity allows you to pivot when markets change, to seize opportunities when others are constrained, or to buy distressed assets when the economy turns dire, often at substantial discounts.

For high-net-worth families, a thoughtful liquidity buffer can be the difference between stability and forced, less favorable decisions. When people talk about wealth, the focus often settles on total net worth—property, business ownership, investment portfolios, and all the impressive numbers that fill a balance sheet. But financial stability is rarely determined by net worth alone. However, what actually protects a family when conditions shift is liquidity.

In practical terms, liquidity is what keeps you flexible, resilient, and positioned to act—not react. It underpins confidence in your financial plan, allowing you to maintain lifestyle stability while still pursuing growth. One simple measure can reveal whether your wealth is truly built on solid ground: the liquidity ratio. This ratio compares your readily accessible resources to your short-term obligations and serves as a clear indicator of how well-prepared you are for both challenges and opportunities.

The Liquidity Ratio: A Simple Formula with Big Implications

Liquidity Ratio = Liquid Assets ÷ Total Net Worth

Liquid assets include cash, money markets, short-term Treasuries, readily tradable, cash-like securities (e.g., select ETFs with short duration) and other immediately accessible holdings.

But liquidity is not limited to cash or CDs. A well-constructed liquidity reserve can include a diversified portfolio of liquid, tradeable securities with layers of conservative, cash-like instruments inside it. This approach allows liquidity to remain readily accessible while still earning a reasonable return. The goal is not money sitting idle—it’s capital that stays available yet productive.

What typically does not count as liquid:

– Private equity and venture positions

– Illiquid real estate investments and development projects

– Restricted or concentrated stock

– Long-hold assets with extended sale timelines

Most financial planning frameworks refer to a 10–20% liquidity target. For many high-net-worth households, that’s just the baseline.

Why High-Net-Worth Families Need More Liquidity Than They Think

Most financial plans use a baseline liquidity target of 10–20% of total net worth. For higher-net-worth families, especially those with sizable real estate, business ownership, or illiquid investments, the practical liquidity cushion often needs to be larger—roughly 15–20% of net worth. Why the uplift? As net worth grows, a greater share of assets sits in structures that don’t readily convert to cash. A deliberate 15–20% reserve preserves optionality without sacrificing long-term growth.

- Real estate beyond the primary residence

- Ownership stakes in private companies

- Business assets used for operations

- Private equity or venture positions

- Concentrated or restricted stock

- Illiquid alternative investments

These assets create paper wealth—yet they offer little help if the need for cash becomes immediate.

This is why the recommended liquidity range for wealthier households rises to 15–20% of total net worth. It’s not arbitrary; it reflects how real-world balance sheets behave during disruptions.

Lessons from 2008–2009: When Credit Lines Vanish and Fire Sales Begin

One of the most painful lessons from the Global Financial Crisis was how quickly “access to liquidity” via credit lines could evaporate — and how dangerous that is for even deeply asset-rich but thinly liquid households or businesses. Capital markets for real estate and other illiquid assets froze or slowed, forcing distress sales and de-risking at unfavorable prices. Even asset-rich, income-rich households found themselves strapped when credit tightened and asset values declined.

- During the crisis, many companies drew heavily on their committed revolving credit facilities. Between 2007 and mid-2009, total drawdowns in some samples rose by around $14 billion, nearly doubling from pre-crisis levels

- At the same time, total revolving lines of credit — the unused lines that firms relied on for contingency liquidity — fell by an amount implying that up to $119 billion of potential credit could not be accessed, per some banking-crisis studies

- That means many firms had committed lines on paper, but in a crisis those lines weren’t fully reliable — banks were under stress, withdrawing or renegotiating their commitments

- On the real estate side, commercial mortgage-backed securities (CMBS) issuance collapsed, and property sales plummeted.

- Vacancy rates rose, property values dropped dramatically (in some segments by 25-50%), and commercial distress mounted as refinancing dried up.

In short: many business owners and real estate investors discovered that their “emergency funding” wasn’t as reliable as they thought — credit lines were becoming less of a cushion and more of a leaky lifeline.

Today’s parallels and why they matter

– Bank lines and credit facilities can tighten quickly in stressed conditions; relying on them as a primary liquidity cushion is risky.

– Commercial real estate refinancing can become challenging as rates rise or values soften.

– Without a liquidity buffer, homeowners and business owners may be nudged toward fire sales or accelerated, suboptimal exits.

– A disciplined liquidity plan helps you ride out volatility without compromising long-term objectives.

That structural stress forced desperate decisions: distressed sales, fire-sales of property, or taking on debt at punishing terms. The very people who felt most secure — asset-rich but illiquid — were uniquely exposed.

Why This Matters for Today — and Why You Need a True Liquidity Buffer

The 2008 experience isn’t just history. Many of the same vulnerabilities exist today:

- Business owners may assume they can lean on bank lines in a crunch. But if systemic stress returns, those lines could be cut or renegotiated.

- Real estate investors, especially in commercial property, may be overly optimistic about refinancing or selling quickly — particularly if values drop or credit tightens.

- Underfunded liquidity means being forced into selling high-quality, long-term assets at unfavorable valuations, just to raise cash.

- Without a buffer, there’s a risk of relying on highly leveraged or operational assets (business, real estate) to provide liquidity — which can destabilize your core wealth in a downturn.

The Quiet Risks Building Today

Several macro conditions echo periods that preceded past liquidity shortages:

- Record-high mortgage and consumer debt

- Commercial real estate facing massive refinancing at higher rates

- Private companies carrying more leverage after years of cheap capital

- A softening US dollar relative to major currencies

- Institutional investors increasing allocations to gold and short-duration instruments

- Margins thinning for small businesses due to labor and supply-chain costs

For any household or business owner relying on borrowing, these trends should serve as a warning: liquidity that feels available today may not be there in the next downturn.

Who Is Most at Risk of Liquidity Shortfalls?

Certain high-net-worth groups are disproportionately exposed to liquidity gaps—even if their net worth appears substantial.

- Real Estate Investors

Particularly those who:

- Hold multiple properties

- Carry significant leverage

- Depend on refinancing cycles

- Hold slow-to-sell properties or commercial assets

Their wealth is tied up in structures, tenants, and debt—none of which can generate immediate liquidity in a stressed market.

- Private Company Owners

Owners of manufacturing firms, professional practices, franchises, logistics companies, and regional services businesses often have most of their wealth locked inside the business.

Cash is constantly reinvested into:

- Inventory

- Equipment

- Working capital

- Employee payroll

- Business growth

These are productive uses of capital—but not liquid.

- CEOs and Small-Business Operators

Even when income is high, liquidity may be low because:

- Expenses scale with revenue

- Capital gets plowed back into expansion

- Payroll and operations consume available cash

- Personal wealth is tied to company equity

These leaders often underestimate how fragile personal liquidity becomes when their firm hits turbulence.

- Entrepreneurs and Growth-Stage Founders

Much of their wealth is:

- In restricted shares

- In illiquid cap tables

- Dependent on future exits

On paper, they may look wealthy. But their liquidity ratio is often dangerously low. Fortunately, we advise clients on accessing illiquid or restricted stock through carefully structured borrowing mechanisms, such as securities-backed lines of credit or margin facilities, allowing them to unlock value without forced sales. By evaluating timing, tax implications, and collateral requirements, we help ensure these strategies enhance liquidity while minimizing risk. This approach provides flexibility to meet cash needs, pursue opportunities, or diversify holdings without compromising long-term investment objectives.

Why the 15–20% Liquidity Standard Matters

For households with substantial home equity, private investments, or business ownership, liquidity is the shock absorber that protects the entire system. The 15–20% target is designed to:

- Provide cash for unforeseen events

- Prevent forced asset sales

- Reduce dependence on bank credit

- Maintain operations during downturns

- Enable opportunistic investing

- Safeguard long-term goals

This level of liquidity supports life transitions, business changes, market volatility, and opportunistic buying without destabilizing the core wealth.

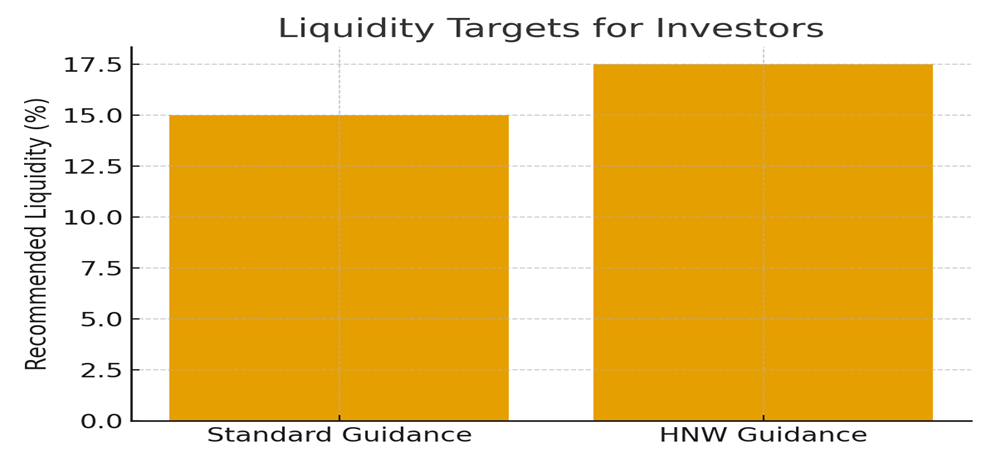

Liquidity Targets at a Glance

Data Snapshot (Illustrative)

Here’s a conceptual breakdown of liquidity targets and tradeoffs:

| Scenario | Recommended Liquidity Target | Why This Matters |

| Typical high-net-worth guidance | ~10–20% of net worth | A broad cushion, but may be insufficient for heavily illiquid balance sheets |

| HNW/private-asset-heavy guidance | ~15–20% of net worth | More realistic when much of your value is in real estate, private companies, or restricted shares |

(Note: These are illustrative; exact targets should be customized based on individual risk profile, asset mix, and liability exposure.)

How Montecito Capital Management Assesses & Delivers on Liquidity Constraints

At Montecito Capital Management, for example, our approach emphasizes preserving optionality. We don’t just optimize for long-term return — we build in the flexibility to act when markets seize up or when once-in-a-cycle opportunities emerge. Part of this process involves carefully identifying areas where cash can be freed up, fine-tuning the overall net worth picture, and establishing an investment framework that balances growth, safety, and liquidity. Further, an advisor can integrate liquidity planning with estate, tax, and philanthropic objectives so liquidity supports all pillars of the family’s plan.

Montecito Capital Management has expertise in designing multi-asset portfolios that include liquid alternative assets, providing insulation against market turbulence while maintaining flexibility. By combining traditional and alternative holdings with liquidity-focused planning, we create a runway that allows clients to navigate uncertainty without resorting to fire-sale decisions — whether that means selling a family business, liquidating real estate, or tapping into illiquid investments at the wrong time.

This disciplined approach ensures that clients have access to the resources they need, when they need them, while still pursuing long-term financial objectives. In essence, liquidity and portfolio design become tools for both security and opportunity — empowering clients to act decisively rather than react to shifting markets.

How a Financial Advisor Can Help

This is where thoughtful financial planning becomes critical. How a seasoned advisor like Montecito Capital Management can help you:

- Set a disciplined liquidity target — not a guess, but a data-informed goal (e.g., the 15–20% of net worth “reserve runway” we’ve discussed).

- Construct a truly liquid portfolio — blending cash-like instruments (short-duration Treasuries, money markets) with more traditional, tradeable liquid securities so your liquidity cushion is both safe and productive.

- Stress-test your balance sheet — running scenarios where credit lines are pulled, markets dislocate, or real estate values drop, to make sure you can survive and adapt.

- Review and rebalance regularly — it’s not a “set it and forget it” exercise. As your business, real estate holdings, and personal balance sheet evolve, your liquidity needs change.

- Position for opportunity — a well-cushioned liquidity runway enables proactive decisions—rebalancing toward growth, capitalizing on dislocations, or quietly acquiring attractive assets when others are constrained.

Conclusion

Liquidity is not a fear-driven precaution; it is strategic capital—an enabler of intentional choices, not a reaction to crisis. By anchoring your plan to a disciplined liquidity target, you preserve optionality, maintain lifestyle stability, and stay positioned to take advantage of compelling opportunities when they arise.

Recall, the 2008–2009 crisis wasn’t just a housing collapse — it was a breakdown of credit reliability. Business lines were pulled. Commercial real estate froze. Many people who thought they had “liquidity commitments” found they didn’t.

For high-net-worth individuals — especially those with significant exposure to private companies or real estate — building and maintaining real, usable liquidity is not just prudent. It’s essential. And partnering with a thoughtful financial advisor such as Montecito Capital Management helps ensure that your liquidity strategy is proactive, resilient, and aligned with your long-term goals.