Author: Kip Lytel, CFA

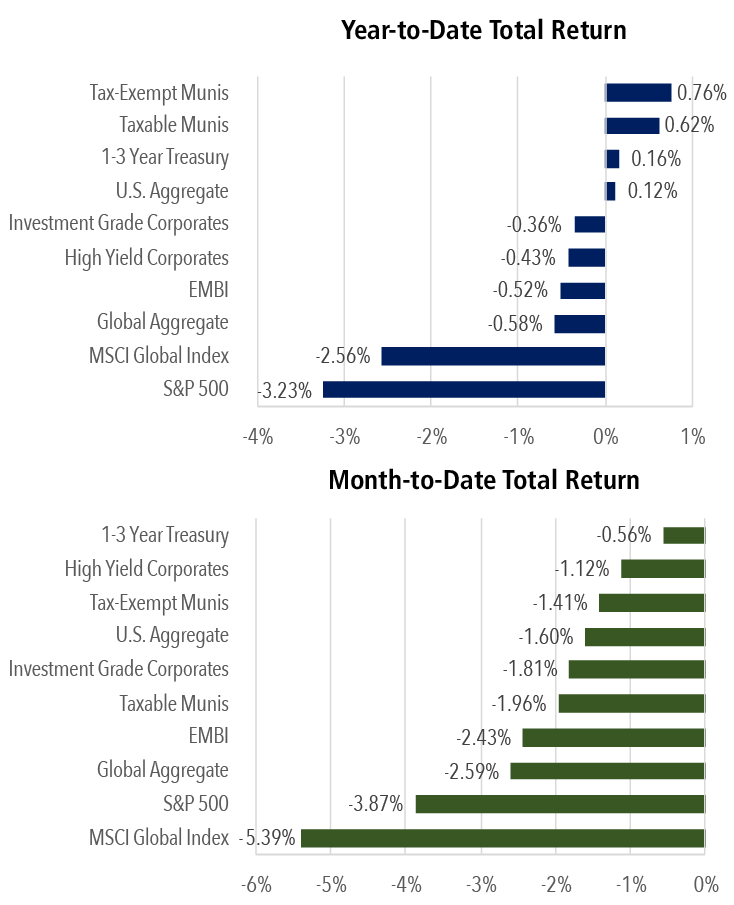

U.S. equities extended their pullback this week, with the S&P 500 declining roughly 1.8%, the Dow Jones Industrial Average falling about 2.0%, and the Nasdaq Composite lower by approximately 2.2%. From their recent highs earlier this year, the major indexes are now down in the range of 5% to 8%, reflecting a steady repricing of risk rather than a disorderly unwind.

At the center of this volatility is the escalating conflict involving Iran, which has become the dominant macro driver across global markets. What had been a relatively contained geopolitical backdrop has quickly evolved into a direct threat to global energy supply, forcing markets to reassess risk across multiple dimensions. The situation has moved beyond headline risk and into tangible economic impact, particularly through energy markets.

Oil has been the primary transmission mechanism. The conflict has disrupted key infrastructure and shipping routes, including critical flows through the Strait of Hormuz, a chokepoint for a significant portion of global energy supply. As a result, crude prices have surged and remain highly volatile, reintroducing a geopolitical risk premium that had largely faded in recent years. This sharp move higher in energy has complicated the inflation outlook, raising concerns that price pressures could reaccelerate just as they were beginning to ease.

That dynamic has driven a shift in interest rate expectations. Markets have moved away from a near-term easing bias and back toward a “higher for longer” stance, as central banks are forced to weigh the inflationary implications of sustained energy strength. Treasury yields have edged higher, tightening financial conditions and pressuring equity valuations, particularly in more rate-sensitive areas of the market.

At the same time, economic data has begun to reinforce a more cautious backdrop. GDP was revised meaningfully lower, with fourth-quarter growth reduced to approximately 0.7%, marking a sharp deceleration from the prior quarter and one of the softer readings in recent periods. The revisions point to weaker underlying demand, with softness across consumer spending, business investment, and trade—suggesting the economy entered the year with less momentum than previously believed.

Importantly, while the current oil spike naturally raises comparisons to 2022, the broader macro backdrop is materially different. At that time, inflation was fueled by an overheated labor market, severe supply chain disruptions, and substantial fiscal stimulus. Today, those conditions have largely normalized. Labor markets remain solid but less tight, supply chains are functioning more efficiently, and fiscal support has diminished. While higher oil prices may create near-term inflation pressure, the risk of a sustained, broad-based inflation surge appears more contained than in that earlier period.

The result is a more complex market environment. Growth is slowing but not collapsing, inflation risks are rising but not yet entrenched, and geopolitical uncertainty—centered on Iran—has become the key swing factor for both.

At Montecito Capital Management, this type of environment is precisely what our portfolios are built for. Our multi-asset, liquid alternative strategies are designed not only to participate in long-term market growth, but to navigate periods of heightened volatility and macro uncertainty. By diversifying beyond traditional stock and bond exposures and incorporating strategies that can adapt across market cycles, we seek to reduce reliance on any single outcome—whether it be falling rates, stable geopolitics, or uninterrupted economic expansion. Importantly, our approach emphasizes flexibility and risk management, allowing us to reposition as conditions evolve rather than remaining static. While short-term market dislocations are inevitable, our focus remains on preserving capital, compounding returns over time, and maintaining resilience through precisely the kinds of shocks currently driving markets.

In sum, this is a market undergoing a classic risk reset, driven by the convergence of geopolitical escalation, energy market disruption, and softer growth. Until there is greater clarity on the trajectory of the Iran conflict and stabilization in oil prices, volatility is likely to remain elevated, with markets highly sensitive to both headlines and macro data.