Author: Montecito Capital Management

The United States has entered a financial period defined by a stark imbalance: the nation now carries more debt than the economy produces in an entire year, and that debt continues to grow faster than the economy itself. This widening gap is not a temporary fluctuation but a structural pattern that increasingly shapes the country’s long-term fiscal outlook. When obligations expand more rapidly than the output that supports them, financial pressure compounds, flexibility shrinks, and the system becomes progressively more fragile.

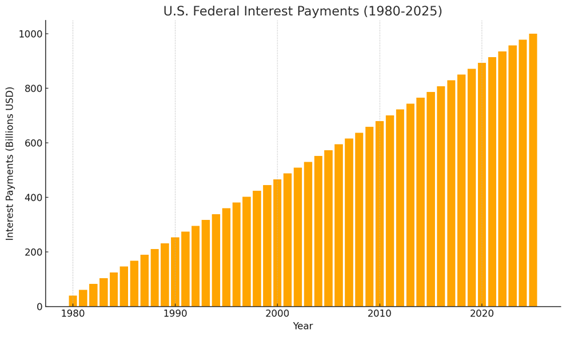

One of the clearest signs of this imbalance is the accelerating cost of interest. At today’s debt levels and interest rates, the federal government pays nearly $1 trillion a year simply to service existing obligations. Every hour, roughly $110 million is spent on interest alone, and each day that figure nears $2.6 billion—money that produces no new infrastructure, no innovation, no stronger national security. It is merely the cost of carrying the past forward, and it grows larger each year.

The U.S. Debt and the Economy: A Ticking Time Bomb Hiding in Plain Sight

America’s fiscal trajectory has reached a point where the numbers themselves tell the story. The federal debt is no longer just an economic statistic; it is the gravitational force pulling on every discussion about national priorities, future taxation, entitlement reform, and market stability. The U.S. is now operating with a debt load that exceeds the size of its economy, and the imbalance is widening each year.

How Big Is the Debt?

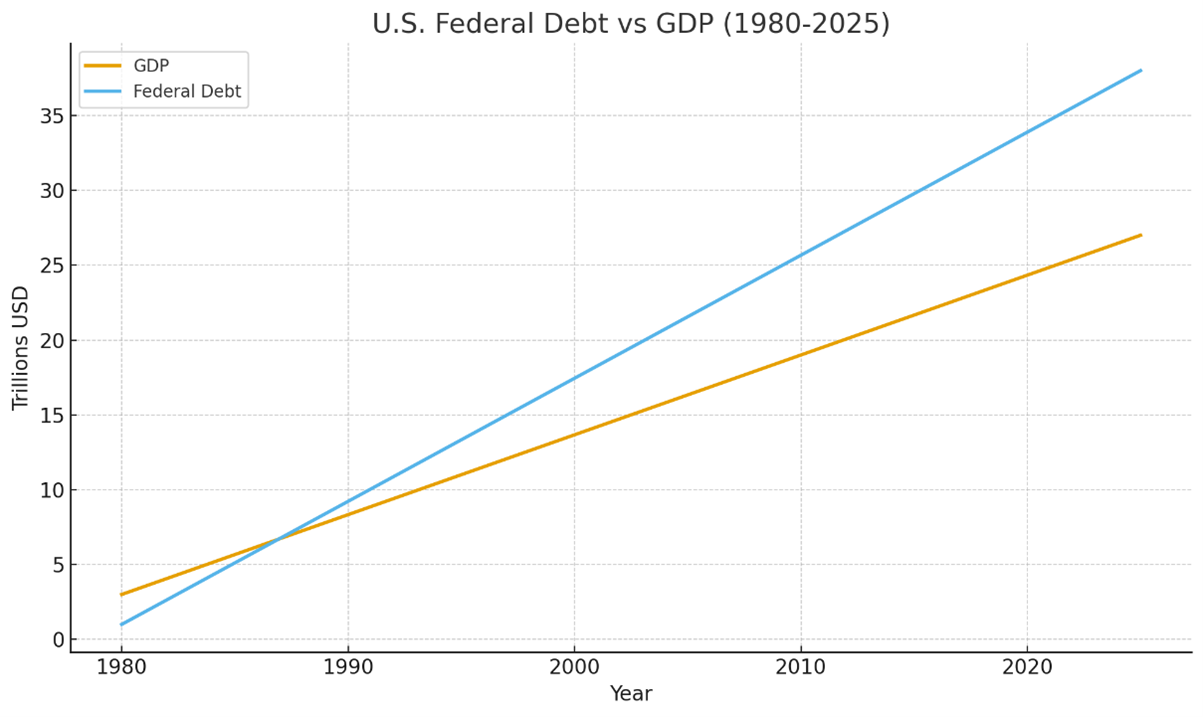

Federal debt has climbed into the $37–38 trillion range. This includes obligations to public investors, pension funds, foreign governments, financial markets, and internal government accounts. It is the cumulative result of decades of structural deficits and compounding interest.

How Big Is the U.S. Economy?

The U.S. economy, measured by nominal GDP, stands around $26–30 trillion. In simple terms, the country produces about $27 trillion worth of goods and services per year—an amount that now falls short of what the nation owes.

The Debt-to-GDP Ratio

This puts the debt-to-GDP ratio at roughly 118% to 124%. In practical terms, the government owes about $1.20 for every $1.00 the economy generates annually. Surpassing the 100% level marks a point where debt becomes heavier to manage and begins crowding out fiscal flexibility over time.

Growth vs. Accumulation: The Structural Imbalance

Economic Growth

Under typical conditions, the U.S. economy grows about 2–4% annually, depending on productivity, labor trends, inflation, and global dynamics.

Debt Growth

Federal debt, however, grows much faster. The government regularly runs deficits exceeding $1 trillion per year, not including interest on accumulated borrowing. This ensures that debt expands more quickly than the economy, deepening the long-term imbalance. Over the past ~20 years (roughly 2005–2024), the U.S. federal debt rose from about $7.93 trillion to about $35.5 trillion, due to both borrowing and interest accrued.

When debt consistently grows faster than GDP, the fiscal burden becomes heavier even if the economy continues to expand. This is the core structural issue facing U.S. finances today.

Why This Path Unsustainable

- Interest Costs Are Exploding

As debt rises, interest payments absorb a growing share of the federal budget. With higher rates, this category has become one of the fastest-growing expenses. The amount of interest accruing, making US debt skyrocket, is approximately $17 billion per week. Funds directed toward interest cannot be used for national priorities.

- Structural Deficits Are Permanent

The federal government spends more than it collects even during strong economic years. Persistent deficits guarantee ongoing borrowing, locking in a long-term upward trajectory for the debt.

- Demographics Add Automatic Pressure

An aging population increases obligations for Social Security, Medicare, and healthcare. These entitlement costs grow automatically and consume more of the budget each year.

- Economic Growth Cannot Keep Pace

If the economy grows at 2–3% while debt grows substantially faster, the ratio worsens over time. Interest and entitlement costs begin to crowd out investments that support future growth.

- Market Confidence Has Limits

The U.S. benefits from issuing the world’s reserve currency, but investor patience is not infinite. If markets demand higher yields to offset perceived risk, borrowing costs rise, accelerating the cycle of debt growth.

The United States is not on the brink of default, but it is on a trajectory that becomes untenable if left unchanged. Debt now exceeds the size of the economy, deficits are structurally embedded, and interest costs are rising rapidly. A nation cannot sustain an environment where its obligations grow faster than its economic capacity indefinitely. Eventually, the system forces a correction—through inflation, reduced spending power, higher taxes, slower growth, or shifts in market behavior.

The math is clear: the current path is not sustainable, and the longer corrective action is delayed, the more difficult the eventual adjustment becomes.

Why Investors Need a Plan if the System Comes Under Stress

Most investors do not track the underlying fiscal pressures—ballooning debt, rising interest costs, weakening fiscal flexibility, and shifting market confidence—until the risks start to materialize. When confidence falters, it is often the average investor who suffers, reacting emotionally or being overexposed to assets vulnerable in a crisis.

This is where a sophisticated advisor becomes essential. Firms like Montecito Capital Management specialize in navigating systemic risks and building portfolios designed to remain resilient even if broader financial conditions deteriorate. Rather than assuming stability will continue indefinitely, Montecito prepares clients for scenarios where fiscal imbalances force adjustments—through inflation, currency shifts, market repricing, or credit stress.

One cornerstone of this approach is maintaining a measured allocation to tangible stores of value. Client portfolios typically include around an 8% allocation to gold and silver ETFs, and having clients hold physical gold/silver assets with no counterparty risk and a long history of retaining value in times of uncertainty.

But precious metals are only one layer of protection. In extreme scenarios, capital often seeks safety in reliable foreign currencies or high-quality sovereign securities. Montecito Capital Management can reposition investments into more stable currency-backed assets when needed, including directly holding Swiss francs, historically a safe haven during global financial stress.

Other “flight to safety” strategies in a severe disruption might include:

• rotating into short-term, high-quality government bills that are geographically diverse

• increase exposure to precious metal ETFs and physical gold

• holding cash or cash equivalents, but prepare to hold in other foreign currencies

• deploying defensive liquid, tradeable alternative strategies to protect capital

• reducing exposure to risk-sensitive sectors or long-duration assets

• maintaining a portion of financial assets outside the domestic financial system in local currency for diversification

• have an sophisticated investment advisor that has a plan and strategy in place to pivot portfolio allocations

These measures are not predictions of catastrophe—they are strategic safeguards. For investors without the tools to interpret large-scale fiscal risks, having a plan with a sophisticated advisor ensures the ability to act decisively and protect wealth should the environment shift suddenly.

What Still Protects the United States from a Full-Blown Debt Crisis

Despite the alarming debt trajectory, the U.S. is not yet on the verge of collapse. Several structural advantages provide a buffer against immediate systemic failure. The United States remains the largest economy in the world, continues to attract the greatest capital flows into innovation and technology, the U.S. dollar remains the world’s primary reserve currency, and American capital markets dominate globally, offering liquidity and depth unmatched elsewhere. These factors allow the U.S. to carry a debt load that would severely constrain other nations, while investors around the world continue to trust the U.S. to honor its obligations, enabling relatively low borrowing costs.

However, these protective advantages are not guaranteed forever. Emerging economies like India and China are growing rapidly, increasing their share of global GDP, investment, and technological development. China, in particular, is projected to continue strong economic growth and may surpass the U.S. in total nominal GDP sometime between the mid-2030s and mid-2040s, depending on growth, productivity, and currency factors. India’s economy is also expanding quickly, leveraging demographic trends and technology adoption to accelerate growth. As these nations catch up, the U.S. could face stiffer competition for capital, trade influence, and currency dominance, gradually eroding the natural buffers that currently protect its debt position.

In short, the U.S. debt problem is partially mitigated today by its size, economic dynamism, and global financial influence—but the rising power of other major economies underscores that these advantages may diminish over time. This makes proactive fiscal planning and strategic portfolio management even more essential, ensuring that both policymakers and investors can navigate a world in which America’s relative economic dominance is no longer guaranteed.