October 25, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The S&P 500 concluded the week with a decline of 1%, representing its first setback following a six-week period of gains. The stock market is facing challenges as renewed uncertainties regarding the Federal Reserve’s interest rate strategy dampen investor enthusiasm for risk. Nevertheless, consumer sentiment has improved for the third month in a row, reaching its highest level since April 2024, as reported by the University of Michigan’s Survey of Consumers. The Consumer Sentiment Index increased to 70.5 in the October 2024 survey, rising from 70.1 in September and surpassing last October’s figure of 63.8. This sentiment is now over 40% higher than the low recorded in June 2022. Tesla emerged as a notable performer following its earnings report, achieving more than a 20% earnings surprise, with gross margins being a frequently highlighted positive aspect. The overall gross margin for the company was 19.8%, an increase from 18.0% in the second quarter and 280 basis points above market expectations.

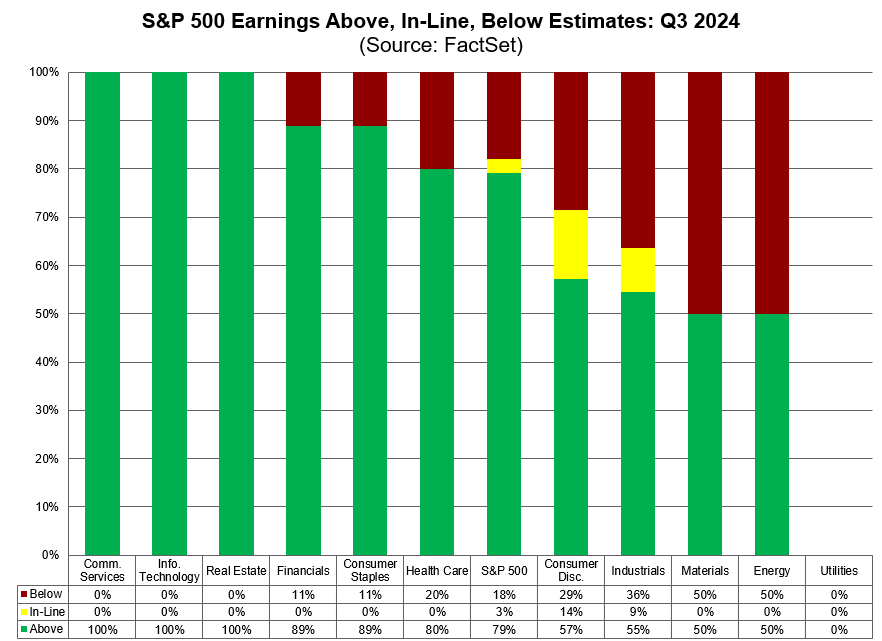

October 17, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. U.S. stock markets experienced an upward trend, achieving new record highs and concluding their longest weekly winning streak of the year. On Friday, the S&P 500 index increased by 0.4%, surpassing the all-time high established earlier in the week and marking its sixth consecutive week of gains. The Dow Jones Industrial Average led the weekly performance with a 0.9% rise, while the Nasdaq Composite followed with a 0.7% increase. According to Factset, 79% of S&P 500 companies have exceeded earnings per share (EPS) estimates for the third quarter, surpassing the five-year average of 77% and the ten-year average of 75%. In labor market news, applications for jobless claims decreased by 19,000 to 241,000 for the week ending October 12, falling well below the anticipated 262,000. This decline follows a significant spike attributed to Hurricane Helene and an ongoing strike involving Boeing machinists. Minneapolis Federal Reserve President Neel Kashkari expressed agreement with the notion of further gradual reductions in the policy rate in the upcoming quarters to fulfill the dual mandate of low inflation and robust job growth. He noted that the Federal Reserve is nearing its goal of reducing inflation to the 2% target.

October 11, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The S&P 500 advanced by 0.6%, achieving its fifth consecutive week of gains, the longest winning streak since May. The Nasdaq increased by 0.3%, and the Dow Jones ended the week with a 1% rise. Strong bank earnings and further signs of a soft-landing trajectory for the economy contributed to the positive performance of US equity markets. The Consumer Price Index (CPI) recorded a 0.2% rise from the previous month, consistent with the increase noted in August and surpassing economists’ forecasts of a 0.1% rise. In September, the CPI rose 2.4% year-over-year, a slight deceleration from the 2.5% annual increase in August. While inflation is showing signs of moderation, it remains above the Federal Reserve’s target of 2% on an annual basis. The key inflation measure indicated that price increases did not ease as much as expected in September, although there has been a notable cooling trend over the last two years. The Federal Reserve has recently begun to concentrate on the labor market, which has demonstrated surprising strength in the context of high interest rates.

October 4, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The three primary indices recorded weekly gains, with the Nasdaq leading the way at +1.25%, while the Dow and S&P 500 saw increases of around 0.8% and 0.9%, respectively. A crucial test for the current rally is imminent as corporate earnings reports are set to be released next week, with investors eager to confirm the high valuation multiples through high level earnings growth. The September jobs report has far surpassed expectations, indicating that the U.S. economy added 254,000 jobs, which has led to a decline in the unemployment rate to 4.1%. Wage growth, an essential metric for evaluating inflationary trends, rose to 4% year-over-year, compared to a 3.9% annual increase in August. The strength of the job market considerably reduces the likelihood of a 0.50% interest rate hike this year, and if the economy continues to demonstrate job growth, the prospect of a 0.25% rate cut may also be eliminated. Historically, in the 16 rate-cutting cycles since 1954, equities have significantly outperformed bonds on average, with small-cap stocks yielding slightly higher returns than their large-cap counterparts.