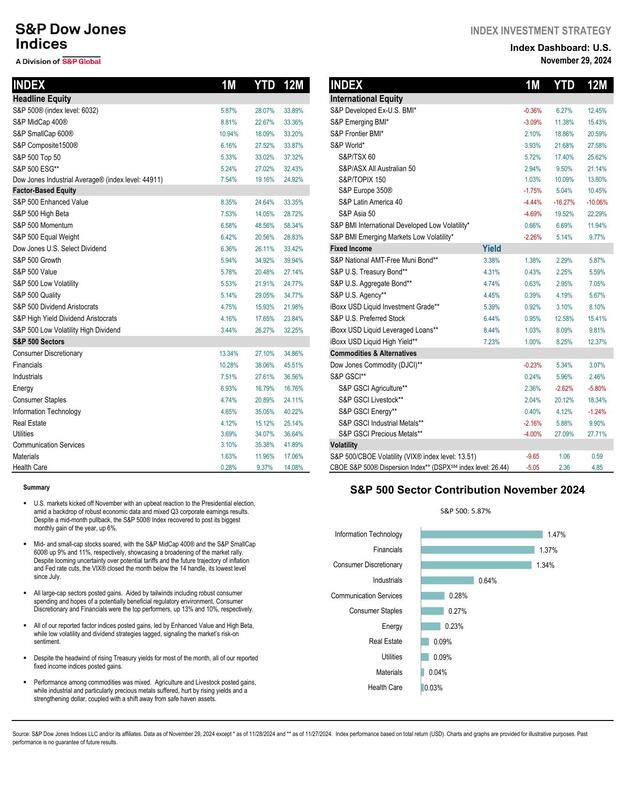

November 30, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. In the holiday-shortened trading week, the Dow recorded a gain of 1.4%, while the S&P 500 and Nasdaq both increased by 1.1%. This rebound in the major indices followed a downturn in October, spurred by positive sentiment regarding Donald Trump’s decisive win in the early-November presidential election. The S&P 500 and Dow Jones wrapped up November with notable monthly increases of 5.7% and 7.5%, respectively, marking their most significant one-month gains of the year. The Nasdaq Composite also saw a rise of 6.2% this month, representing its best performance since a 6.9% increase in May. Traders are anticipating a 25 basis point reduction in borrowing costs by the U.S. central bank at its December meeting, although they expect a halt in rate cuts in January, according to the CME Group’s FedWatch.

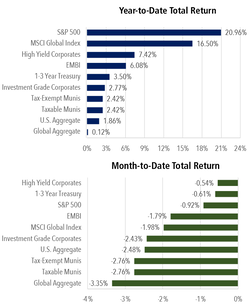

November 15, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. This week, all three major indexes experienced declines. The Dow Jones Industrial Average fell by 1.2%, while both the S&P 500 and Nasdaq recorded their largest weekly drops since September, decreasing by 2.1% and 3.2%, respectively. The most significant losses were observed in the technology sector, as investors reacted to disappointing earnings reports and concerns regarding the sector’s vulnerability to rising interest rates. Federal Reserve officials indicated that further rate cuts next month may not occur as previously anticipated. Notably, on Friday alone, the market capitalization of the six most valuable companies in the S&P 500—Nvidia, Apple, Microsoft, Amazon, Alphabet, and Meta—dropped by $458 billion. Both Amazon and Nvidia saw their market values decline by over $90 billion each. Additionally, major pharmaceutical companies such as Moderna, Pfizer, and AstraZeneca faced declines on Friday following the nomination of Robert F. Kennedy Jr., a vaccine skeptic, by Trump for the position of health and human services secretary. Although retail sales data released early Friday exceeded expectations, suggesting positive economic conditions, it also reinforced the notion that the Federal Reserve may not be as aggressive in reducing its benchmark interest rate as some investors had hoped. Federal Reserve Chair Jerome Powell noted on Thursday that ongoing economic growth, a robust job market, and inflation rates above the central bank’s 2% target justify a cautious approach to future rate cuts.

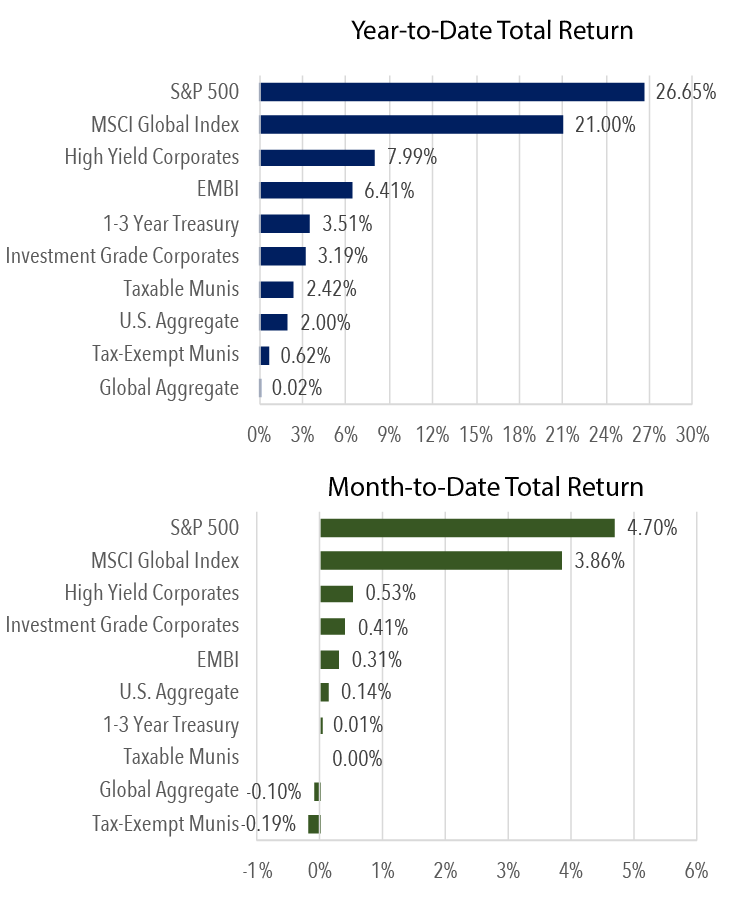

November 8, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The S&P 500 briefly crossed the 6,000 level and finished the week with its largest weekly percentage increase in a year, spurred by Donald Trump’s election win and the prospect of a Republican sweep in Congress, which raised hopes for favorable business policies. For the week, the S&P 500 recorded a gain of 4.66%, the Nasdaq rose by 5.74%, and the Dow increased by 4.61%. Trump’s election as President of the United States ignited a significant rally in the dollar, drove stock indices to all-time highs, and negatively impacted bond prices, as expectations for tax cuts and tariffs on imports fostered optimism regarding economic growth while also raising inflation concerns. The anticipated deregulation, tax reductions, and growth-oriented policies were pivotal in the market’s positive response. Sectors likely to benefit from Trump’s victory include traditional energy, defense, real estate investment trusts (REITs), and financial stocks, including those related to blockchain and cryptocurrencies. Trump is expected to reverse regulatory measures and advocate for the oil, gas, and coal sectors. Furthermore, he is likely to implement tax reductions for businesses, which should favor financial stocks, while his stance on cryptocurrencies is also positive. Given Trump’s longstanding support for a robust military, defense stocks are expected to perform well. Additionally, the Federal Reserve announced a quarter-point reduction in interest rates on Thursday. “This is a process that requires time,” stated Powell during a press conference following the Fed’s decision to lower its benchmark overnight interest rate to a range of 4.50%-4.75%. “We continuously assess the net effect of all policy changes on the economy at any given moment. This is a process we engage in with every administration.”

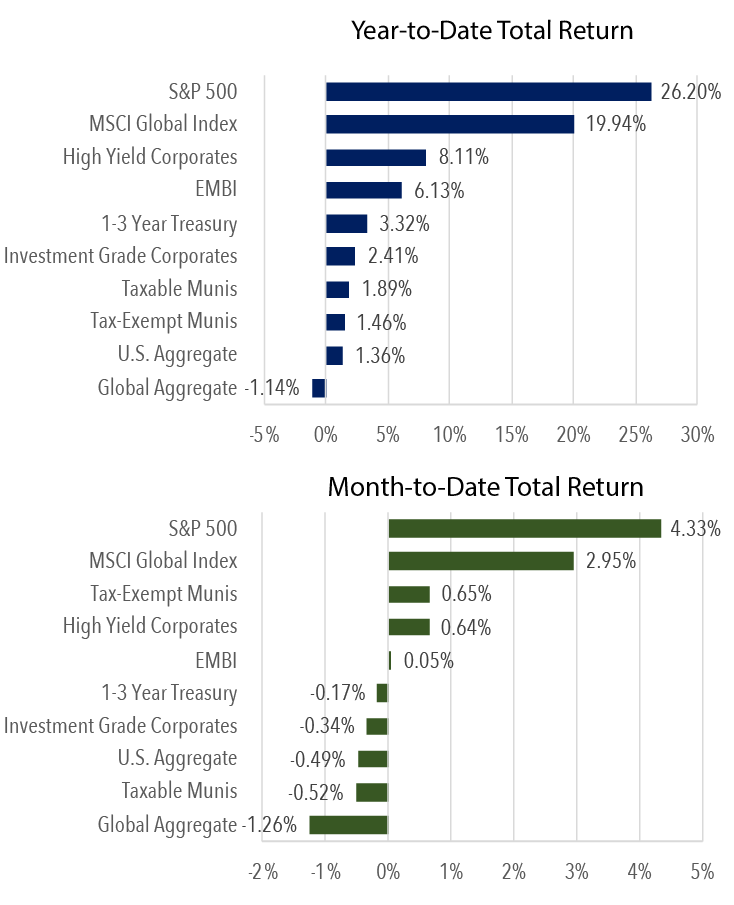

November 1, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The S&P 500 index experienced a decline of 1.4%. The Nasdaq composite, which reached a record high on Thursday morning, fell by 1.5%, thereby ending a seven-week streak of gains. Recent data from Wealthmanagement.com’s monthly Advisor Sentiment Index for September indicates that confidence in the economy has risen by three points to 103, moving slightly into positive territory from last month’s neutral reading of 100. On Friday, the Labor Department reported that the economy added a seasonally adjusted 12,000 jobs in October, a significant decrease compared to the September increase of 223,000. Economists surveyed by The Wall Street Journal had anticipated a gain of 100,000, factoring in the impacts of storms and strikes. Both indexes concluded the month with slight losses. Job growth decelerated considerably last month, influenced by the effects of hurricanes and the ongoing Boeing strike. Nevertheless, the unemployment rate remained stable at 4.1%, aligning with economists’ forecasts. The market’s attention is now centered on the possibility of a rate cut or a pause as it approaches next week. Two pivotal reports will influence the Federal Reserve’s decisions in November. These options are currently under consideration for central bank policymakers at their upcoming meeting on November 6-7, with this week’s reports on inflation and the labor market potentially affecting the final decision. The Fed is already on track for a 25-basis point rate cut in November and is unlikely to change this course, regardless of the incoming data. As of last Friday, investors were pricing in over a 90% likelihood of a 25-basis point rate cut during the Fed’s meeting on November 6-7.

November 1, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The S&P 500 index experienced a decline of 1.4%. The Nasdaq composite, which reached a record high on Thursday morning, fell by 1.5%, thereby ending a seven-week streak of gains. Recent data from Wealthmanagement.com’s monthly Advisor Sentiment Index for September indicates that confidence in the economy has risen by three points to 103, moving slightly into positive territory from last month’s neutral reading of 100. On Friday, the Labor Department reported that the economy added a seasonally adjusted 12,000 jobs in October, a significant decrease compared to the September increase of 223,000. Economists surveyed by The Wall Street Journal had anticipated a gain of 100,000, factoring in the impacts of storms and strikes. Both indexes concluded the month with slight losses. Job growth decelerated considerably last month, influenced by the effects of hurricanes and the ongoing Boeing strike. Nevertheless, the unemployment rate remained stable at 4.1%, aligning with economists’ forecasts. The market’s attention is now centered on the possibility of a rate cut or a pause as it approaches next week. Two pivotal reports will influence the Federal Reserve’s decisions in November. These options are currently under consideration for central bank policymakers at their upcoming meeting on November 6-7, with this week’s reports on inflation and the labor market potentially affecting the final decision. The Fed is already on track for a 25-basis point rate cut in November and is unlikely to change this course, regardless of the incoming data. As of last Friday, investors were pricing in over a 90% likelihood of a 25-basis point rate cut during the Fed’s meeting on November 6-7.

October 31, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. In October, the Dow Jones Industrial Average, S&P 500, and Nasdaq all recorded monthly losses. The Nasdaq was particularly affected, leading a decline in U.S. stock markets on Thursday, as earnings from Meta (META) and Microsoft (MSFT) raised apprehensions about the outlook for major technology firms amid escalating artificial intelligence expenses. On that day, the Nasdaq fell by 2.7%, while the S&P 500 experienced a nearly 1.9% decrease on October 31, 2024.