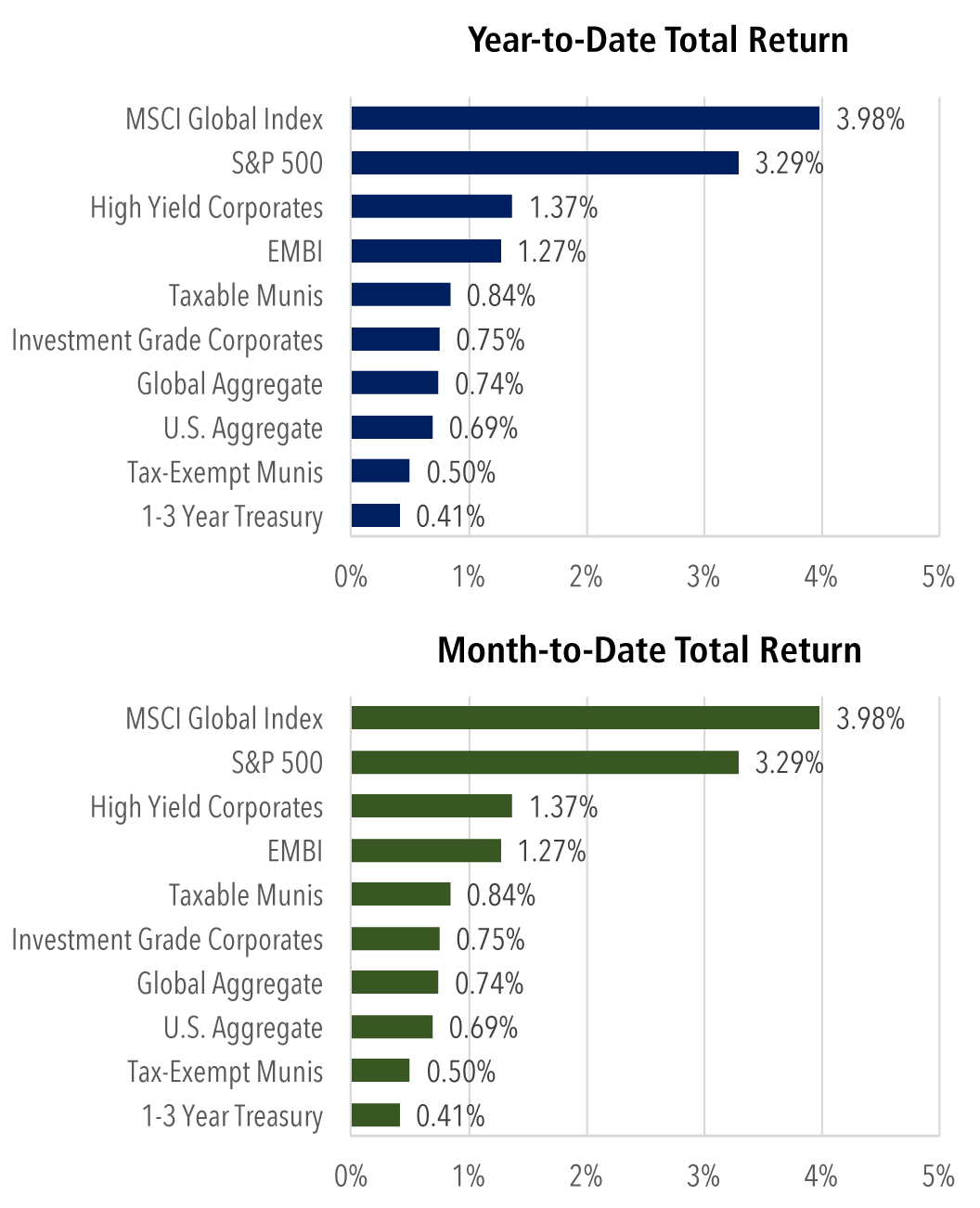

February 21, 2025, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. Stocks experienced a reversal of their weekly gains on Friday as investors became more cautious in response to signs of an underperforming economy. The Dow and Nasdaq fell by 2.5%, while the S&P 500 Index saw a decrease of 1.7% for the week. The University of Michigan reported that consumer sentiment in February dropped to 64.7 from 67.8 earlier in the month, reaching its lowest level since November 2023. This decline represents nearly a 10% decrease from January. Further compounding worries were indicators of weaknesses in the service industry, with declining retail sales, and a 4.9% decline in existing home sales last month.

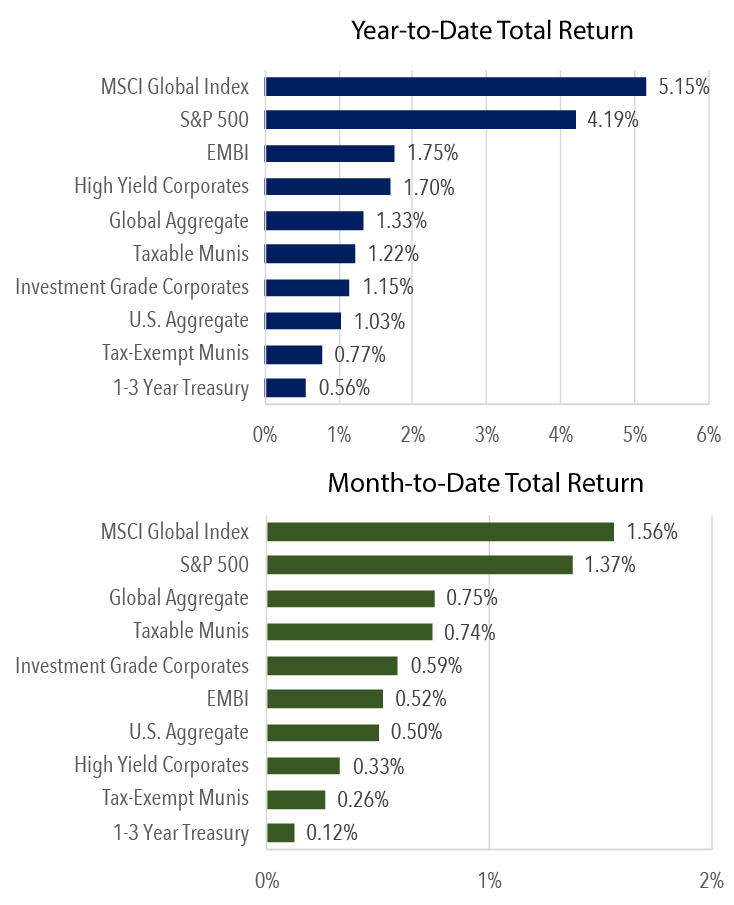

February 14, 2025, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. This week, the Nasdaq distinguished itself with a notable increase of 2.5%, securing the title for the largest gain, while the S&P 500 index experienced a rise of 1.6% over the past five days. The Dow Jones also saw a modest increase of 0.7%. A stronger-than-anticipated inflation report has led investors to reassess their expectations regarding interest rate reductions in 2025. The Consumer Price Index (CPI) for January, released on Wednesday, indicated that overall consumer prices rose more than expected, with core prices reversing the previous month’s decline. On a core basis, which excludes the more volatile food and energy prices, January saw a 0.4% increase compared to the previous month, surpassing December’s growth. Federal Reserve Chair Jerome Powell emphasized a cautious approach to interest rates during his testimony before the Senate Banking Committee, stating, “With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance.” Additionally, U.S. producer prices showed a solid increase in January, reinforcing the notion that inflation is on the rise and bolstering market expectations that the Federal Reserve will refrain from cutting interest rates before the latter half of the year. According to the Labor Department’s Bureau of Labor Statistics (BLS), the producer price index for final demand rose by 0.4% last month, following an upwardly revised 0.5% increase in December, while economists had anticipated a 0.3% rise. Furthermore, retail sales experienced their most significant decline of the year, dropping by 0.9% in January, exceeding the expected 0.2% decrease, marking the largest month-over-month drop in retail sales since January 2024.

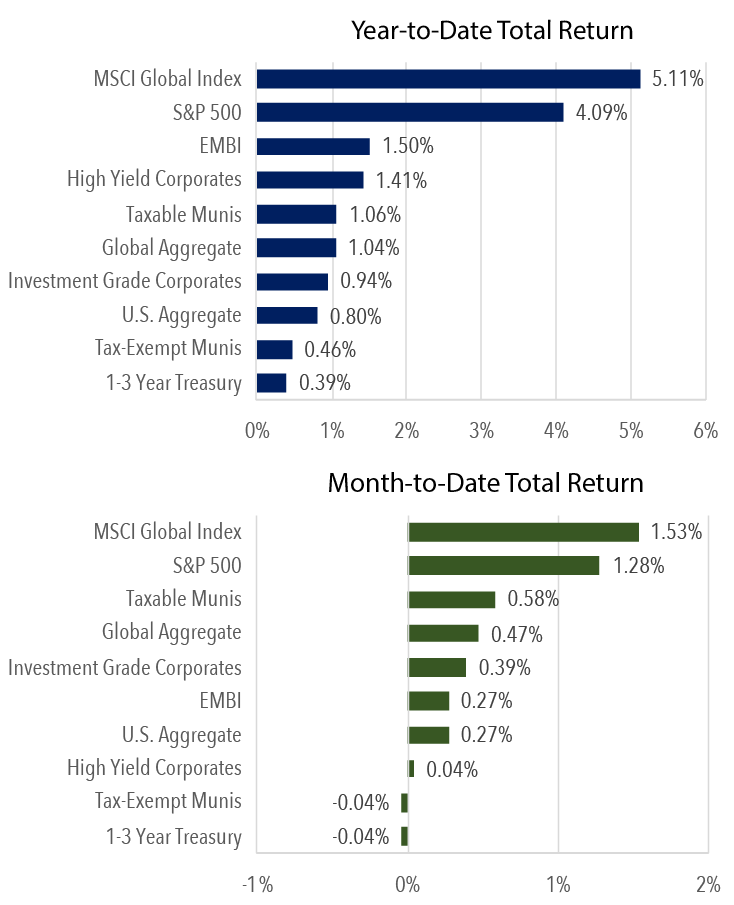

February 7, 2025, Weekly Stock Market Return Recap, by Kipley Lytel CFA, Montecito Capital Management. The week ended with all three major U.S. stock indices closing lower, following a series of erratic trading sessions driven by tariff-related trade uncertainties and notable earnings from major technology firms. The principal indices finished in the negative, with the Dow Jones and Nasdaq each declining by 0.5%, while the S&P 500 saw a slight reduction of 0.2%. The Labor Department’s employment report released on Friday morning revealed that job growth in January was less than what economists had anticipated, although the unemployment rate surprisingly fell to 4.0%. The monthly jobs report is a critical indicator that the Federal Reserve uses in its interest rate deliberations, making it an essential data point for investors. Additionally, the 2-year treasury rate increased by 7.1 basis points, closing at 4.28%, the highest closing figure since January 23rd.

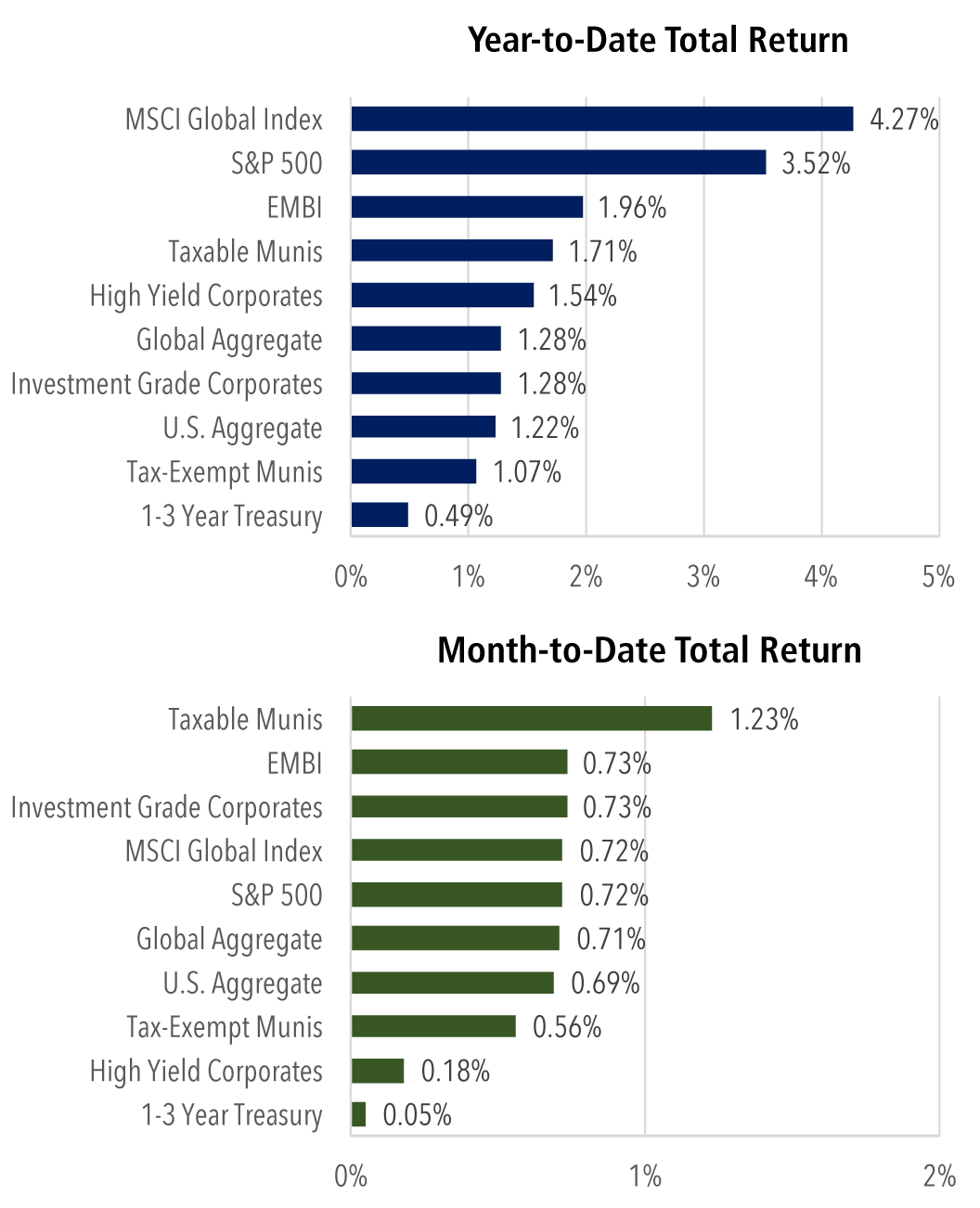

January 31, 2025, Weekly Stock Market Return Recap, by Kipley Lytel CFA, Montecito Capital Management. On the week, the S&P 500 experienced a decline of 1%, while the Nasdaq, which is heavily weighted towards technology, saw a more significant drop of 1.6%. In contrast, the Dow Jones Industrial Average recorded a slight increase of 0.3%. On Monday, global investors responded by offloading technology shares, fearing that the launch of an affordable Chinese artificial intelligence model could threaten the dominance of leading AI companies like Nvidia (NVDA). This resulted in a remarkable loss of $593 billion in Nvidia’s market capitalization, marking the largest single-day drop for any firm on Wall Street. In a widely expected move, the Federal Reserve decided to hold interest rates steady after three consecutive cuts, marking the first pause since July 2024. The Federal Open Market Committee reached a unanimous consensus to maintain the target federal funds rate within the range of 4.25% to 4.5%. Policymakers reiterated their dedication to assessing “the extent and timing” of any future rate changes based on evolving data and forecasts. They also noted that the unemployment rate has “stabilized at a low level in recent months,” in contrast to earlier descriptions of it having “eased,” and confirmed that job market conditions remain “solid.” The U.S. economy recorded slower-than-expected growth in the fourth quarter, with the Bureau of Economic Analysis’s preliminary estimate showing an annualized growth rate of 2.3%, which is below the 2.6% growth anticipated by economists surveyed by Bloomberg. The Personal Consumption Expenditures Price Index experienced a rise of 0.3% in December, marking the most significant increase since April of the previous year, following an unchanged gain of 0.1% in November, as reported by the Bureau of Economic Analysis within the Commerce Department. Year-on-year, PCE inflation has increased by 2.6%.