December 27, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. Despite a notably poor performance on Friday, the S&P 500 and Nasdaq both achieved a weekly gain of 1.8%, while the Dow Jones recorded an increase of 1.5%. U.S. consumer confidence dropped to its lowest point since September, with a December reading of 104.7, down from November’s 111.7 and below the expected 113.2. While new jobless benefit applications in the U.S. have remained consistent, claims have surged to a three-year high. The Dot Plot forecast anticipates only two rate cuts in the forthcoming year, while projecting a core PCE inflation rate of 2.5%. This indicates that the Federal Reserve expects inflation to remain elevated for an extended period, making significant interest rate reductions unlikely, contrary to earlier market expectations this year. Much of the stock market rally anticipated in 2024 was based on the belief that the central bank would continue to relax monetary conditions in the coming quarters.

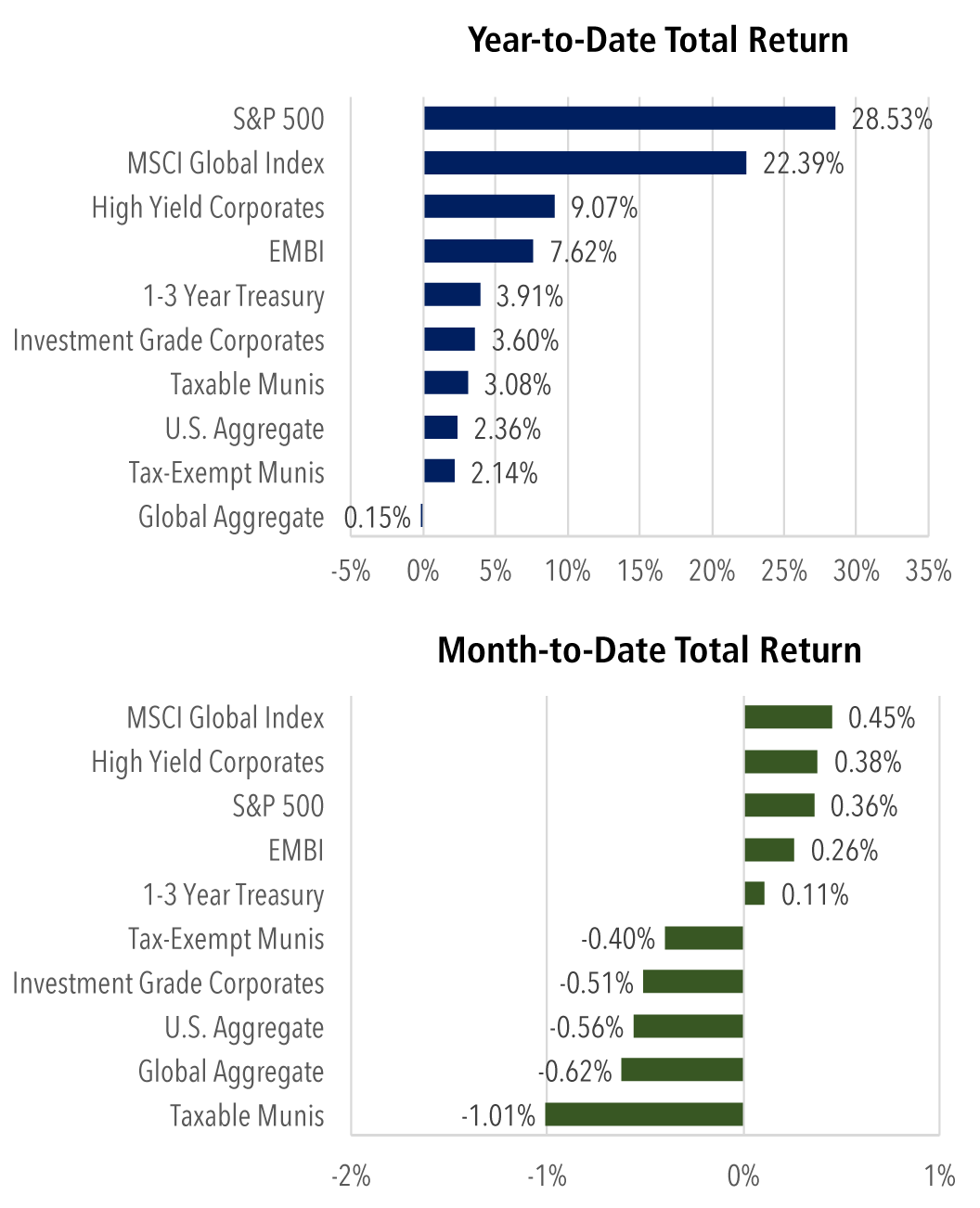

December 20, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The Federal Reserve (“Fed”) opted to lower interest rates while suggesting that fewer rate reductions are in store ahead for 2025. Though the S&P 500 saw a 1.1% increase on Friday, ending an 11-day losing streak, it still recorded a 2% decline for the week. The Dow Jones fell by 2.3%, and the Nasdaq experienced a 1.8% decrease over the same timeframe. On Wednesday, the Federal Open Market Committee decided to cut the federal funds rate by a quarter-point, marking its third consecutive reduction, which now places the rate within the range of 4.25% to 4.50%. This decision was largely expected, even in light of ongoing inflationary pressures and a strong economy and job market. Furthermore, Fed officials have revised their unemployment projections for 2025 downward and have updated their inflation forecast for that year to 2.5%, an increase from the 2.1% forecast made in September. The latest figures from the Fed’s preferred inflation measure revealed that while month-over-month price increases decreased in November, inflation remains persistent as the central bank strives to achieve its 2% target. In November, the core Personal Consumption Expenditures (PCE) index, which excludes food and energy prices and is closely monitored by the Fed, increased by 0.1% compared to the previous month, a slowdown from the 0.3% rise observed in October.

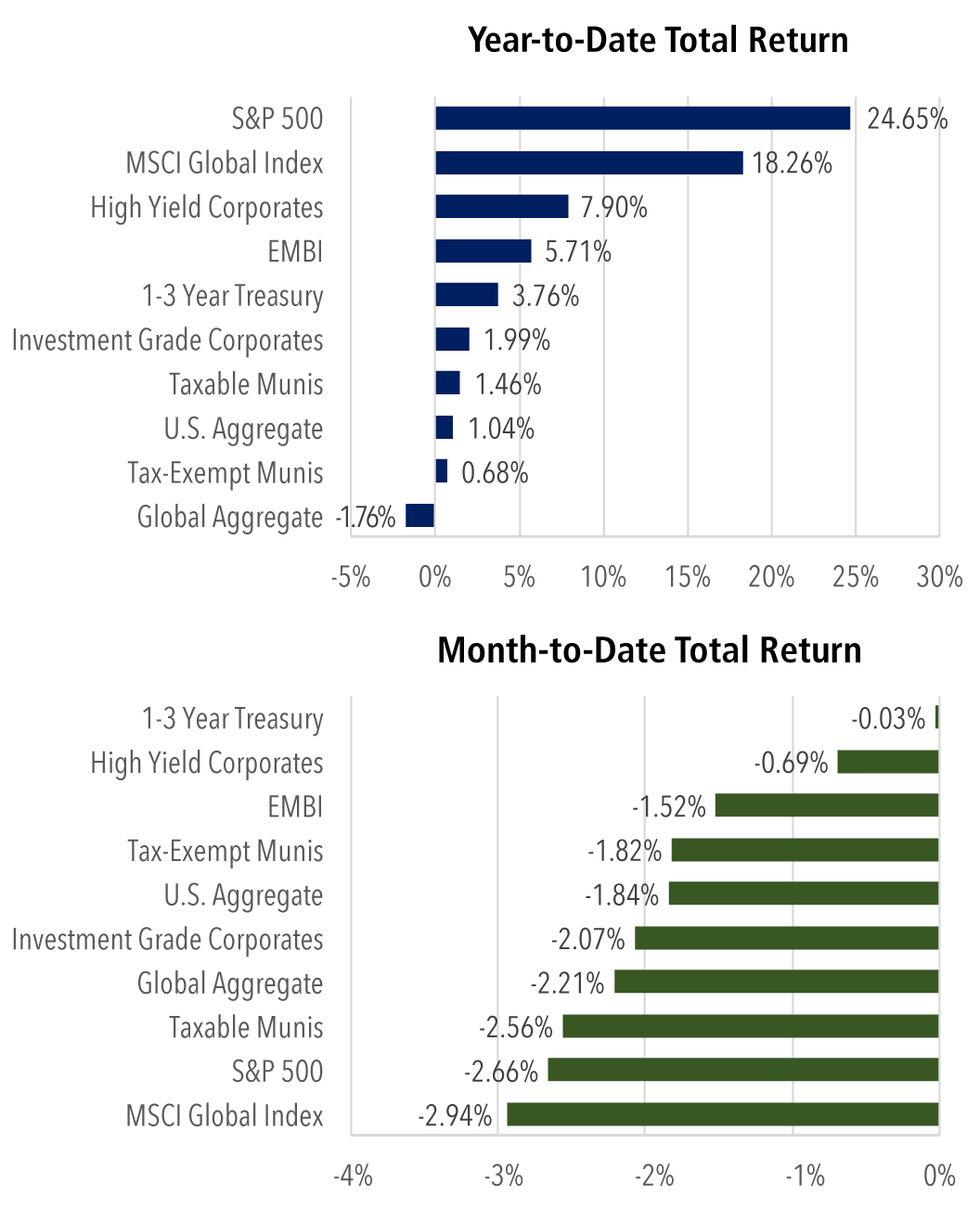

December 13, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The trading week concluded with U.S. stocks showing mixed results: the S&P 500 and Dow Jones both recorded weekly declines, while the Nasdaq marked its fourth consecutive week of gains. Specifically, the Dow experienced a 1.8% drop, and the S&P 500 decreased by approximately 0.6%, thus ending a three-week upward trend. Conversely, the Nasdaq posted a gain of 0.3%. On Wednesday, inflation data revealed that consumer prices rose in November as anticipated, which may keep the Federal Reserve on track to consider interest rate reductions in December. The Consumer Price Index (CPI) increased by 2.7% year-over-year in November, reflecting a slight uptick from October’s annual increase of 2.6%, which was in line with economists’ forecasts. Following the U.S. presidential election, consumer sentiment has shown signs of improvement, as indicated by surveys from the University of Michigan and the Conference Board. Furthermore, the National Federation of Independent Business reported on Tuesday that its small-business optimism index surged in November, reaching its highest point since June 2021. A subsequent report from the Bureau of Labor Statistics on Thursday indicated that the producer price index (PPI), which tracks price changes faced by businesses, rose by 3% year-over-year, an increase from October’s 2.4% and exceeding the expected 2.6% rise. However, when food and energy are excluded, the core PPI increased by 0.2%, aligning with expectations, while an adjustment for trade services resulted in a minimal 0.1% rise. Despite ongoing inflationary pressures, market participants largely expect the Federal Reserve to lower its key overnight borrowing rate in the coming week.

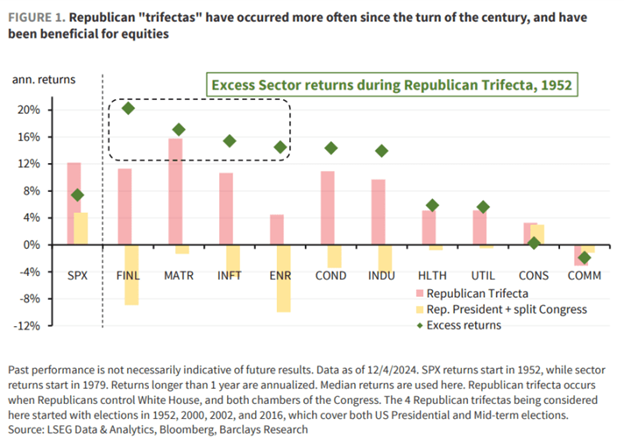

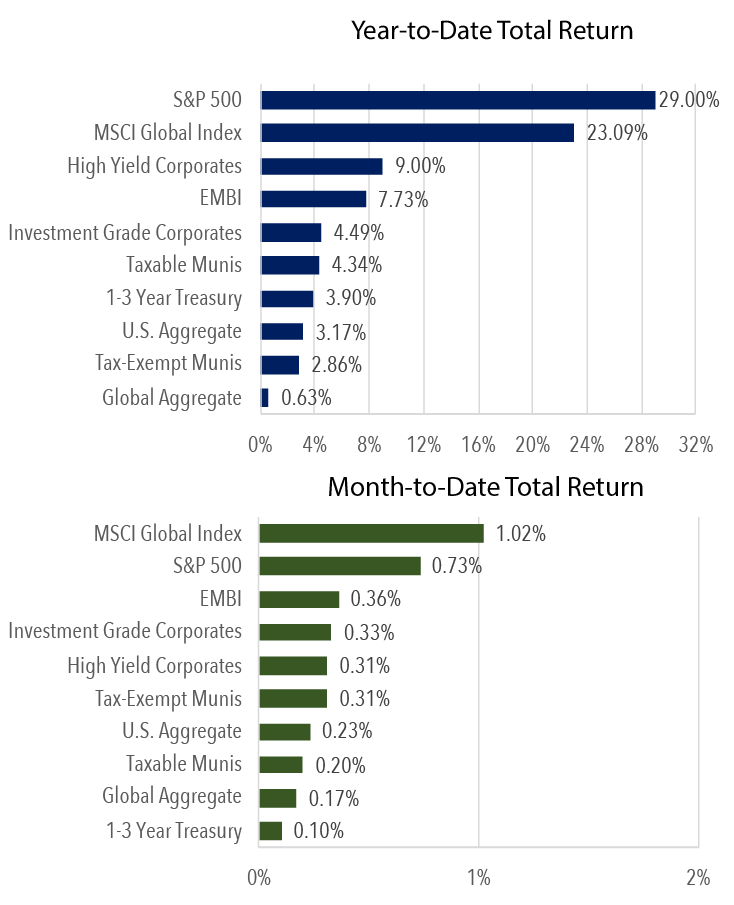

December 6, 2024, Weekly Stock Market Return Recap, by Kip Lytel CFA, Montecito Capital Management. The S&P 500 and Nasdaq Composite reached new all-time highs on Friday, buoyed by November employment figures that were slightly better than anticipated, yet not strong enough to dissuade the Federal Reserve from potentially lowering interest rates again later this month. As a result, both indices enjoyed their third consecutive week of positive performance, with the S&P 500 rising by 0.96% and the Nasdaq by 3.34%. Conversely, the Dow saw a decrease of 0.6% during this period. The Nasdaq, which is heavily weighted towards technology, increased by 0.81% to close at 19,859.77, driven by gains in major tech firms such as Tesla, Meta, and Amazon. According to Barclays, historical trends show that stocks tend to outperform when the Republican Party holds unified control of the U.S. government.