Skip to content

Skip to content Author, Montecito Capital Management

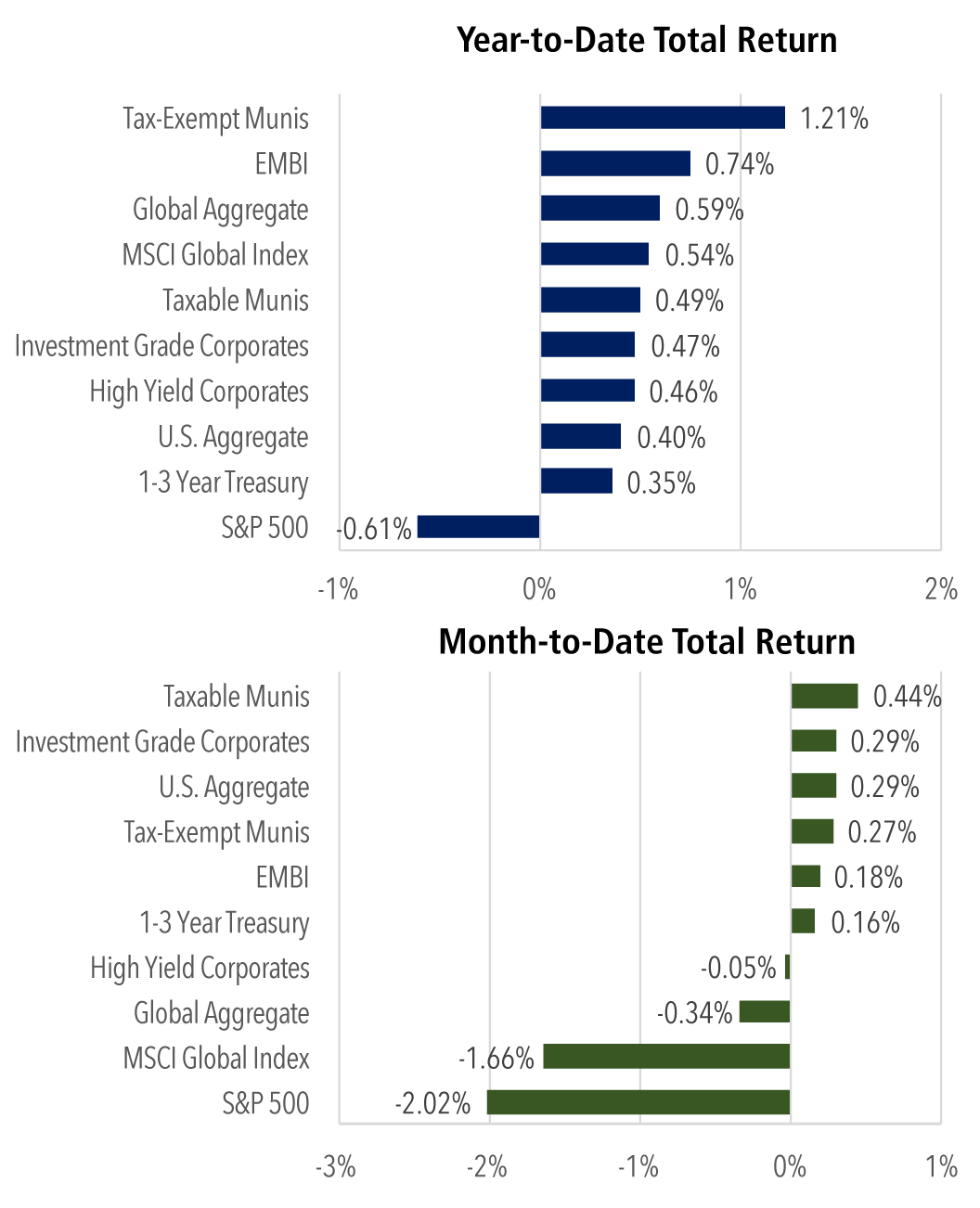

For the week ending February 6, U.S. equities delivered a split verdict. The Dow Jones Industrial Average advanced solidly, supported by rotation into cyclicals and industrial leadership, while the S&P 500 hovered around flat and the Nasdaq Composite declined as pressure on high-multiple growth names outweighed strength elsewhere. Beneath the surface, the tape was far more volatile than those headline numbers suggest. Markets swung between enthusiasm around resilient economic momentum and anxiety that the next phase of the AI build-out may demand more time and capital before fully translating into earnings power.

The turbulence was most visible in software. By Thursday, many technology names had experienced drawdowns approaching 12% for the week even as hyperscalers posted impressive revenue growth and surprised to the upside with aggressive capital expenditure plans. In prior quarters, that combination would have ignited a broad rally. Instead, investors hesitated.

We can point to several reasons.

First, the debut of Claude’s autonomous AI agent — able to operate directly within the browser — sharpened fears that increasingly capable AI systems could disintermediate portions of traditional software. If models can execute workflows themselves, what happens to the application layer? Add to that the expectation that surging hyperscaler spend will rapidly improve performance, and you have the ingredients for a classic disruption scare.

Second, the market is wrestling with a timing issue. AI investment is undeniable; the revenue realization curve is less so. When capital intensity rises faster than near-term monetization, multiples tend to compress until visibility improves.

Our interpretation is more constructive.

History suggests platform shifts rarely eliminate the need for software; they redefine it. AI does not remove the requirement for security, governance, integration, compliance, customization, and workflow orchestration — it increases it. Enterprises will still buy systems of record and systems of engagement, but those products will be infused with intelligence and priced for the productivity they unlock.

Likewise, hyperscale capex should be viewed as the groundwork for future demand. More compute, better models, and lower unit costs expand the addressable market. That typically precedes, rather than coincides with, the acceleration in application-layer revenue.

Friday’s rebound reinforced the point. Buyers stepped back into select growth franchises while money continued to rotate into areas tied to tangible economic activity, reminding investors that this is a broadening market rather than a collapsing one.

The takeaway from the week is not that the AI thesis is broken. It is that we are moving from excitement about possibility toward scrutiny of execution, durability, and return on invested capital. That transition can be uncomfortable in the short run, but it is ultimately what builds the foundation for the next sustained advance.